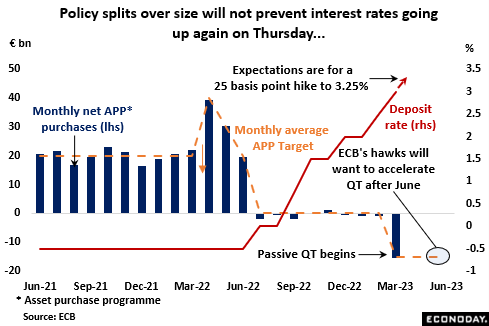

With inflation still misbehaving and the global banking sector at least more stable, market expectations are for yet another hike in key ECB interest rates this week. However, in line with the March meeting, a reasonably broad consensus on the Governing Council (GC) about the need to tighten masks clear disagreements over the extent to which rates need to go up. In contrast to the February announcement, the March statement provided no specific forward guidance leaving forecasters pondering a smaller 25 basis point increase versus another 50 basis point move. The consensus is 25 basis points which would put the (still key) deposit rate at 3.25 percent, its highest level since November 2008, the refi rate at 3.75 percent and the rate on the marginal lending facility at 4.00 percent. It would also boost the cumulative tightening since last July to some 375 basis points.

Passive QT began in March when the central bank allowed a net €15.4 billion of maturing assets to run off its balance sheet, essentially meeting the average €15.0 billion monthly target that runs through June. Some €10.1 billion of disposals from the public sector purchase programme (PSPP) accounted for much of the decline followed by a €2.8 billion reduction in holdings in the corporate sector purchase programme (CSPP). However, with only partial re-investment having had minimal impact on bond spreads and the current stock of QE still more than €3.2 trillion, a number of GC hawks have called for the pace of QT to be stepped up significantly from July. Indeed, at the current rate, the PSPP will not be fully exhausted until 2041. A decision on this is unlikely to be made until the June meeting when a revised set of economic forecasts will be available but investors will be watching on Thursday for any hints of a more aggressive stance to come. Recall that the base case projections made in March left both the headline and core inflation rates still above the 2 percent target over the entire forecast horizon, implicitly signalling that policy was still too loose.

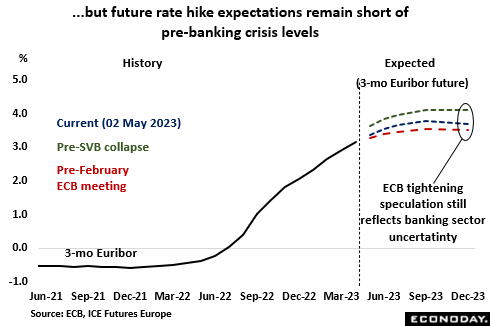

Even so, financial market pricing for future tightening remains more modest than just before the collapse of Silicon Valley Bank (SVB). At that time, futures saw 3-month money rates rising to above 4.0 percent in December but, by the March ECB meeting, the anticipated peak to rates had been cut to around 3.5 percent. Notwithstanding the recent issues with First Republic Bank, the subsequent broad stabilisation of the banking sector has seen the anticipated high creep back up to about 3.8 percent but this is still 30 basis points or so short of its pre-SVB crisis level.

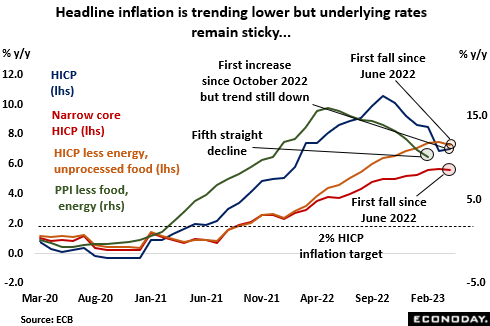

Inflation developments since the last ECB meeting have been mixed. Today’s flash data put April’s headline yearly rate at 7.0 percent, up from a final 6.9 percent in March and its first increase since peaking at a record 10.6 percent last October. However, while remaining unacceptably high, the core rates for one eased a little. The narrowest measure dipped a tick to 5.6 percent, its first drop since June 2022, while omitting just unprocessed food and energy the rate was down 0.2 percentage points at 7.3 percent. Less optimistically, services (5.2 percent after 5.1 percent) continued to accelerate but at least pipeline pressures in manufacturing have eased with the annual core PPI rate having fallen from fully 16.0 percent in May 2022 to 10.2 percent most recently. This still leaves a sizeable gap with its consumer price counterpart but declining selling price expectations in both services and, in particular, manufacturing, last month bode well. On the EU Commission’s measure, consumer inflation expectations have also fallen markedly since the middle of last year and in April matched their lowest level since October 2020.

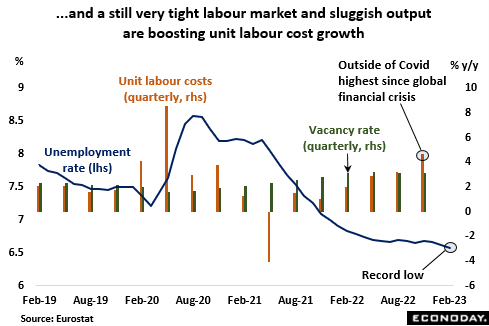

Not helping inflationary matters is the labour market where slack is increasingly hard to find. Joblessness in February fell a further 59,000 which, following a sharply revised 54,000 drop in January, left the unemployment rate at 6.6 percent, a record low and 1.4 percentage points beneath its level just before the arrival of Covid. Vacancies are historically very high and many businesses are clearly reluctant to shed staff even in the face of sluggish demand. This is adding to upside pressure on wages and hence, output prices as firms try to protect real profit margins. Such a combination raises the risk that domestically generated inflation could remain too high even as external factors, notably energy prices, help to reduce the headline rate. This is particularly true of service sector industries where backlogs are still climbing and both input and output prices continue to increase sharply. Consequently, labour market indicators in general remain a key input into ECB policy.

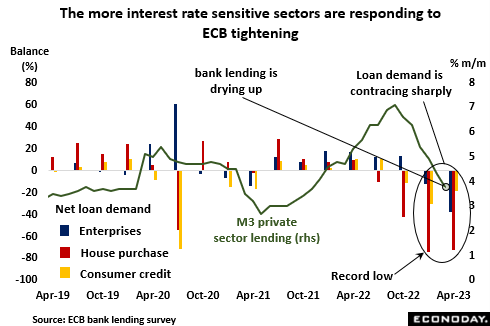

First quarter Eurozone GDP was weak, expanding by a minimal 0.1 percent on the quarter and showed that even if employment has yet to respond to higher interest rates, monetary tightening is impacting the more interest rate sensitive sectors of the economy. Total private sector loan demand has decreased sharply and lending has contracted in three of the last four months. Hence, in March, annual growth of non-financial corporate borrowing was the slowest in 12 months while loans to households for house purchases expanded by the least since December 2018. Official Eurozone house price data are released only quarterly and after a sizeable lag but as of the end of 2022, the region’s annual inflation rate had fallen from a 9.8 percent peak in the first quarter of 2022 to just 2.9 percent, its lowest reading in seven years. Indeed, at minus 3.6 percent, the national rate in Germany was negative for the first time since the end of 2020. Moreover, the ECB’s new lending survey released earlier found banks tightening their lending standards significantly and expecting another contraction in loan demand this quarter.

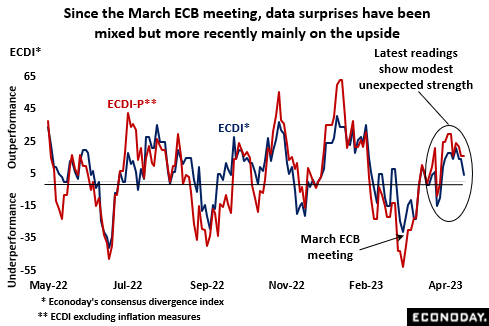

More generally, economic indicators released since the March ECB meeting have been mixed, surprising on both the upside and downside. However, the latest data have typically been on the firm side of expectations and have kept Econoday’s consensus divergence index (ECDI) fairly consistently above zero. That said, with the latest inflation surprises on the downside, the pressure on the ECB to hike has at least eased a little.

To this end, Thursday’s announcement could well see a reduction in the pace of monetary tightening. With inflation at current levels, the ECB’s job is far from done and a 25 basis point hike in key rates might not sit well with the GC hawks. Still, a promise of more aggressive QT next quarter could help to smooth ruffled feathers and even a smaller hike now need not preclude more aggressive rate increases later should inflation fail to behave itself over coming months.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2026 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.