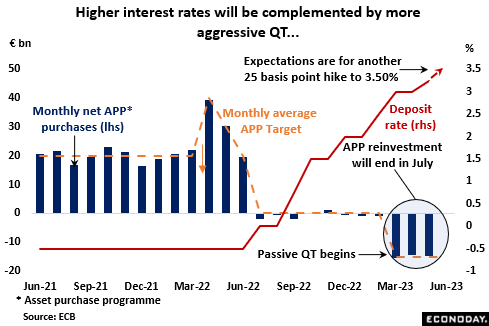

Almost without exception, official comments since the May policy meeting have indicated that Governing Council (GC) members think key interest rates need to be higher if inflation is to be brought back under control. This clear bias has left investors anticipating another 25 basis point hike on Thursday which would put the deposit rate at 3.50 percent, its highest level since November 2008, the refi rate at 4.00 percent and the rate on the marginal lending facility at 4.25 percent. It would also boost the cumulative tightening so far to fully 400 basis points in less than a year.

As well as higher borrowing costs, Thursday’s announcement is likely to confirm an impending step-up in the pace of balance sheet reduction. QT has been running, in passive form, with an average target of €15 billion a month since March. Through the end of May, disposals amounted to slightly more than €50 billion, mainly reflecting a €41 billion fall in holdings under the public sector purchase programme (PSPP). Importantly, to date the sales have had minimal impact on sovereign bond spreads which the GC hawks may well argue as justifying an early switch to active QT (outright sales). As it is, the last month’s meeting indicated that the current policy of partial reinvestment of maturing assets acquired under the asset purchase programme (APP) would be terminated at the start of July. This should roughly double the rate at which these assets are offloaded. However, the pandemic emergency purchase programme (PEPP) continues to lie outside of the QT programme and the GC can be expected to reaffirm that full reinvestment here will run until at least the end of next year.

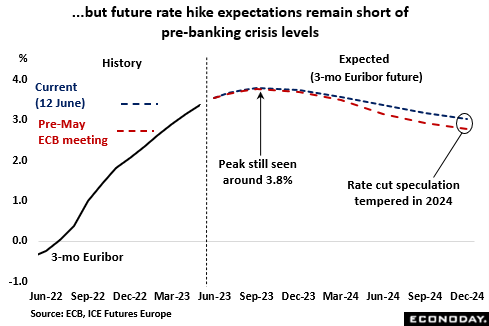

Financial markets currently see the peak to 3-month money rates around 3.8 percent in September, little changed from just before the May ECB meeting but well down from the near-4.1 percent level priced in just before the collapse of Silicon Valley Bank (SVB). However, expectations for ECB easing have been tempered and rates are now seen only marginally lower by the end of this year and still above 3 percent in December 2024.

Recent inflation developments have been a little more positive but will still be viewed as supportive of additional tightening. On the optimistic side, headline inflation has fallen every month since peaking at 10.6 percent last October and, at a surprisingly low 6.1 percent, in May recorded its lowest level since February 2022. However, much of the deceleration was attributable to the negative base effects caused by sharply rising energy costs over much of last year. The underlying picture was more mixed. The May data revealed a sizeable, and much-needed, 0.3 percentage point fall in the narrow core measure to 5.3 percent, matching its weakest mark so far in 2023. However, it was still only 0.4 percentage points short of March’s record high and nowhere near the 2 percent target. That said, inflation in services, currently a key indicator for the ECB, dipped for the first time since last November and the GC’s doves may interpret this as a sign that earlier policy tightenings are now feeding through into prices. The central bank’s new inflation forecasts, also released on Thursday, should make for especially interesting reading.

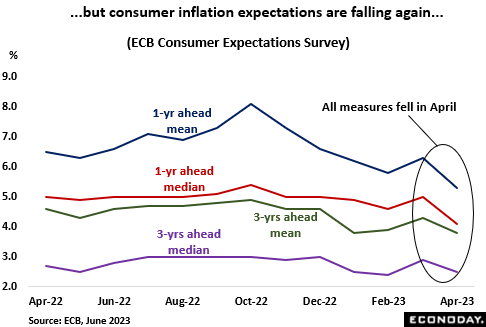

Importantly too, following a notable increase in March, household inflation expectations are falling again. The ECB’s survey released last week showed declines in all the main measures and, apart from the 3-years ahead median, the drop more than reversed the previous month’s rise. The EU Commission’s economic sentiment survey told much the same story for May with selling price expectations in manufacturing and services declining to levels not seen since November 2020 and October 2020 respectively. Household inflation expectations also dropped to their lowest mark since October 2021. The bank follows these (and other) measures closely so the latest developments should increase the chances of a less hawkish tone than in May.

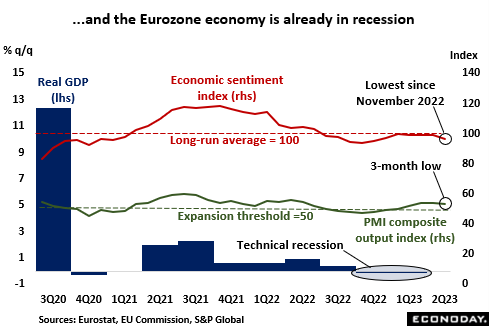

Meantime, last week’s GDP revisions left the Eurozone economy in technical recession as both the final quarter of 2022 and the first quarter of 2023 saw total output dip 0.1 percent. In large part this was attributable to Germany which, after a 0.3 percent contraction last quarter also found itself in recession alongside Estonia, Ireland, and Lithuania. Elsewhere, performances were mixed but, in the aggregate, the region is struggling in the face of declining domestic demand with the consumer sector especially soft. Hence, retail sales volumes in May matched their second lowest level since April 2021. Services have benefitted to some extent from pent-up demand caused by earlier Covid restrictions, but having slumped a monthly 4.1 percent, industrial production in March was the weakest since October 2021. Moreover, in general leading indicators offer only limited hope of any meaningful near-term improvement. At 52.8, May’s PMI composite output index slipped to a 3-month low and that masked the worst performance by the manufacturing sector in fully three years. The EU Commission’s economic sentiment index painted a similarly lacklustre picture, as do the financial data within which narrow money M1 is currently contracting at the fastest pace on record.

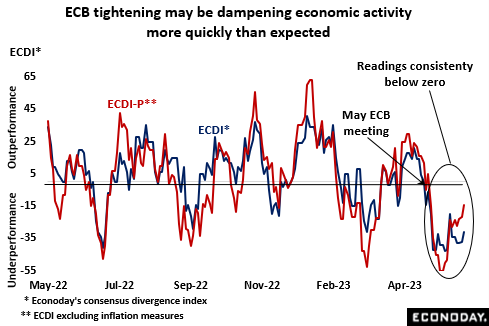

In fact, economic indicators in general released since the May ECB meeting have been surprisingly weak. Econoday’s consensus divergence index (ECDI) was sub-zero over the entire period meaning that forecasters have been consistently too optimistic. Earlier hopes that growth was holding up much better than originally expected now seem less well founded and on current trends, overall economic activity this quarter will also be disappointingly soft. From a policy perspective, the interest rate outlook remains crucially tied to inflation so negative ECDI readings may not seem too important. However, sustained sub-par economic activity must eventually weigh on prices and so bolster the chances of a faster slowdown in core inflation.

As the ECB noted in last month’s bulletin, the bottom line is “the inflation outlook continues to be too high for too long.” As such, another 25 basis point hike in key interest rates this week would appear to be nailed on. However, the May data offer hope that policy is finally beginning to work, notably in the consumer sector and housing market. Indeed, with recession, albeit only very mild at this stage, already in place, the risk of monetary overkill is rising steadily and the debate about what to do with policy at the next meeting in July could well be even more heated than usual.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.