Investors are split on this month’s BoE MPC announcement but the majority call is for no change. The August reduction in Bank Rate to 5.0 percent only got through by the tightest of margins (5-4) with Chief Economist Huw Pill voting against the move and Governor Andrew Bailey stressing the need for careful easing going forward. Still, with inflation down again and wage growth slowing, a small minority of forecasters anticipate a second 25 basis point reduction that would put Bank Rate at 4.75 percent, its lowest level since June 2023. Indeed, potentially increasing the chances of a cut is the arrival on the MPC of Professor Alan Taylor, formerly Professor of International and Public Affairs at Columbia University, New York. Having replaced hawk Jonathan Haskel who wanted no change in August, his vote could prove very important.

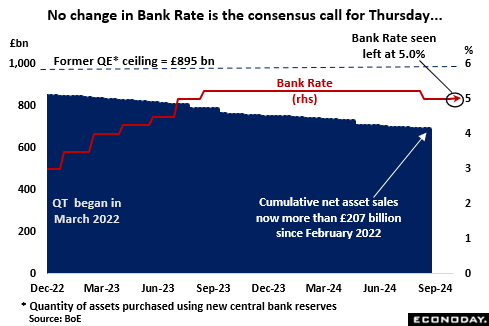

Meantime, QT is due for updating as the current programme is now approaching the end of its target period. In total, net asset disposals have successfully shrunk the bank’s balance sheet by more than £207 billion to £688 billion since February 2022 and Thursday’s announcement should include the new target for gilts for the coming 12 months. The neutral choice would be to retain the existing yearly run-off rate of £100 billion but the decision is complicated by a much heavier gilt maturity calendar in 2025. This means that retaining the current target would imply reducing actual bond sales from around £50 billion in 2024 to only about £13 billion. Conversely, selling the same quantity of bonds would mean shrinking the balance sheet more rapidly. The decision, and the rationale behind it, could have implications for how financial markets react.

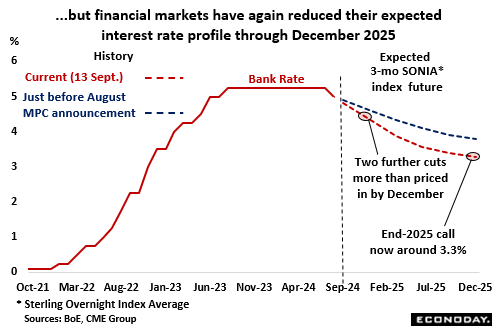

In any event, financial markets now see even more room for interest rate cuts over the medium-term. A 25 basis point reduction this week is not fully priced in but in excess of 50 basis points of easing is now seen by December. By the end of 2025, SONIA is currently put at 3.3 percent, down nearly 50 basis points versus the view held just before the July MPC meeting.

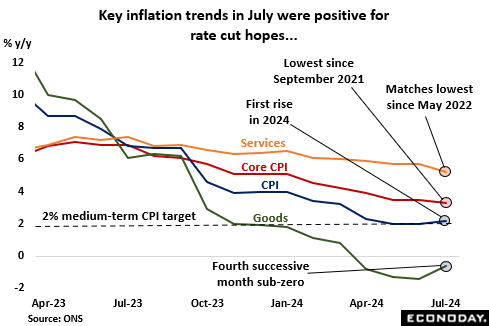

Headline inflation accelerated above target in July but, at 2.2 percent, only slightly and by less than expected. More importantly anyway, the core measure eased a couple of ticks to a 34-month low of 3.5 percent and the rate in the key services category fell fully 0.5 percentage points to 5.2 percent. The latter clearly remains well above 2 percent but the magnitude of its latest decline – the steepest since August last year – will boost hopes that price pressures in the sector are finally beginning to subside. The August CPI report is not scheduled for release until Wednesday, the day before the MPC’s announcement, but early signs look favourable. In particular, the British Retail Consortium found shop prices falling 0.3 percent on the year, their first annual decline since October 2021. Non-food goods were down by 1.5 percent, their largest drop in more than three years.

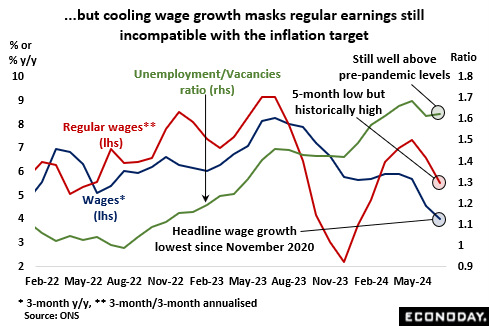

The earnings picture has been mixed. On the positive side, both headline and regular wages have continued to decelerate since the last MPC meeting. Indeed, at 4.0 percent, the overall measure stands at its weakest rate since November 2020. However, the bank’s preferred metric which uses the annualised 3-monthly change in the regular component is still worryingly firm. At 5.1 percent, it remains well above the levels compatible with hitting the inflation target on a sustainable basis. Other labour market indicators similarly offer varied implications. The official jobless rate dropped to a 6-month low of just 4.0 percent in the three months to July and a 265,000 jump in employment was the steepest since March-May 2022. Against that, vacancies have been trending steadily down for two years now and the unemployment/vacancies ratio remains historically high.

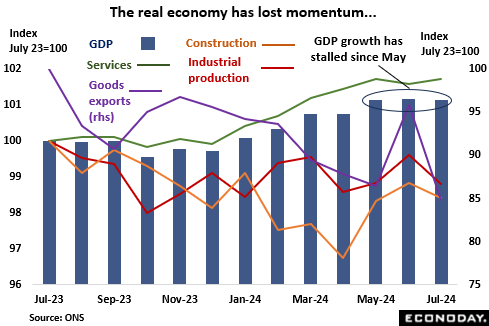

Following a solid start to the year, the economy has recently run out of steam. At 0.6 percent, second quarter growth looked respectable enough but total output has not actually expanded since May. The recovery in industrial production remains painfully slow and with construction volatile, services still shoulder most of the burden. Moreover, although second quarter export volumes increased for the first time since the fourth quarter of 2022, they were still swamped by imports to the extent that net foreign trade subtracted more than 2 percentage points from GDP growth. Goods exports in July were down nearly 16 percent on the year. That said, most leading indicators at least point to a modestly positive near-term outlook and what seems to be a strengthening housing market in anticipation of further cuts in mortgage rates could give a boost to consumer confidence.

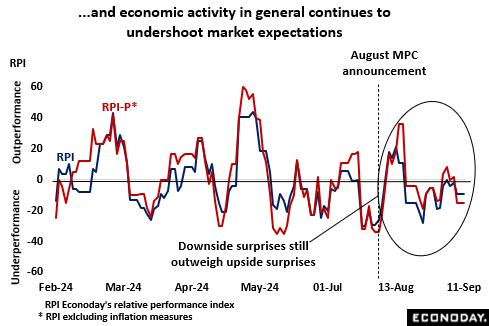

In fact, since the middle of August, overall economic activity has continued to lag market expectations. Over this period, Econoday’s Relative Performance Index (RPI) averaged minus 11 and, excluding inflation indicators (RPI-P), minus 7. Both readings were in negative surprise territory, albeit not by much, meaning that recent economic data in general have been more supportive of the MPC’s doves than hawks.

In a nutshell, the September MPC meeting will need to choose between levels and trends. Current headline, core and service sector inflation rates are all above target and wage growth remains high. However, against that, underlying trends seem to be moving in the right direction. For the doves, delaying another cut would be seen as increasing the risk of monetary overkill while the hawks will worry that another reduction now could be premature and stoke up price pressures further down the road. Consequently, Thursday’s announcement may well be another very close call and market uncertainty about the outcome should mean that asset prices react whatever the outcome.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.