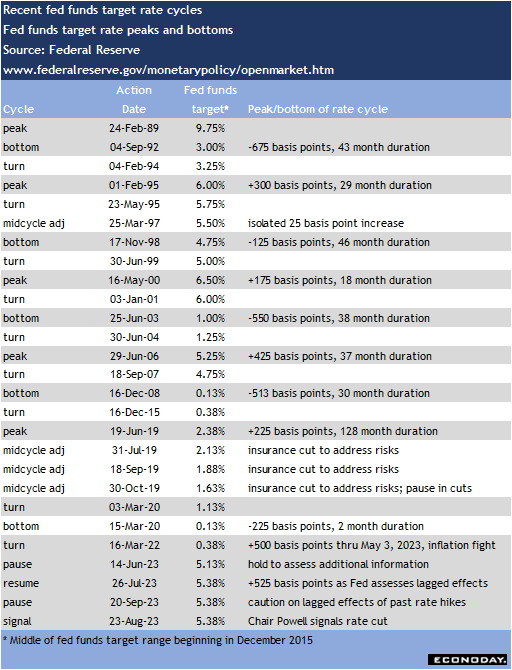

Fed policymakers will always say that no decision is made until they actually meet and consider all the most recent information available. However, they have strongly signaled that they are leaning toward cutting rates at the September 17-18 FOMC meeting. Absent a seismic event for the economy, there should be the first change in in the fed funds target rate range since the current fed funds rate of 5.25-5.50 percent in July 2023.

It is by far most likely that the cut will be 25-basis points. There has been talk of a 50-basis point cut and indications by a few Fed officials that it isn’t out of the question. While the larger cut will be on the table, the majority of policymakers will prefer a smaller cut to start with. The decision will be based on some explicit and some implicit reasons.

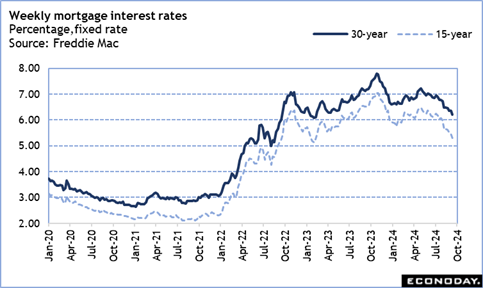

First, financial conditions have already eased significantly in recent weeks as seen in falling mortgage rates. Markets have done some of the work in easing restrictive policy which in turn should make the case for a larger rate cut less urgent.

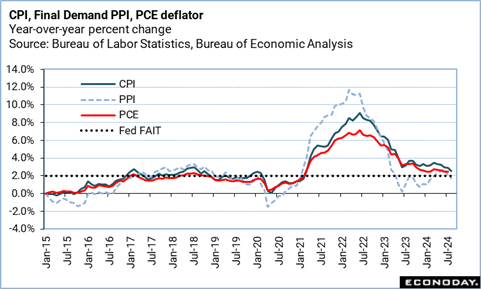

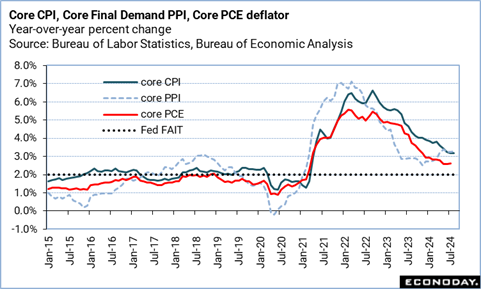

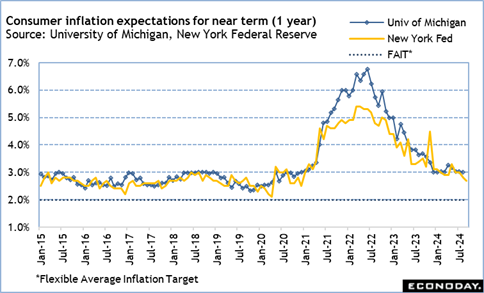

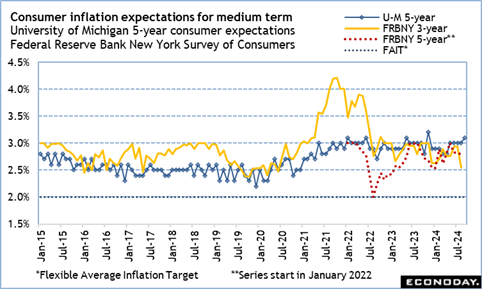

Second, the most recent readings on inflation expectations show that these are not coming down as rapidly for the medium term as they have for the near term. This will counsel the FOMC that the work to sustainably restore price stability is not yet done, especially for prices in non-housing services and shelter costs. Monthly inflation measures are showing more rapid deflation at the all-items level while upward price pressures stubbornly persist at the non-housing services level and for shelter costs.

Third, the FOMC is not panicking about the cooler labor market data. The committee sees labor market conditions as having rebalanced and normalized for an economy in modest growth. Nonetheless, the assessment of risks to the outlook has shifted to a weaker jobs market. A rate cut is appropriate but does not need to be a big one with US GDP running north of 2 percent growth in early forecasts for the third quarter 2024. A soft landing does not require a hard change of direction.

Fourth, it would be naïve to say that the FOMC is setting policy without taking the political climate into account. It will be in the back of their collective thinking that an aggressive rate cut at this time could be misconstrued as seeking to have an impact on the outcome of the presidential election in November when even a 25-basis point cut is already being viewed with suspicions as timed to help one party over another. In the end, a cut that has been well communicated in advance of the meeting and that is supported by the economic data in terms of the Fed’s dual mandate is both the correct action for monetary policy and the least risky.

But what else?

At this meeting the FOMC will update its collective quarterly forecast in the summary of economic projections (SEP). Although Fed officials will again have to reiterate that the contents of the SEP are not a promise of future monetary policy decisions, any change in the forecast for the midpoint of the fed funds target rate is going to get a lot of scrutiny.

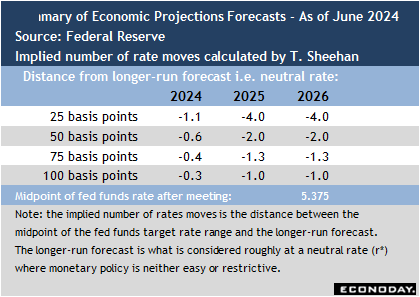

The projections materials released at 14:00 ET on Wednesday along with the post-meeting statement could well reset the tone of the outlook for rates in the remainder of 2024 and into the next few years. The June 2024 SEP forecast roughly one 25-basis point cut in the second half of the year with some possibility of a second cut. The September SEP could well lift that expectation to at least one more 25-basis point cut this year and might even leave open the possibility of another one. The other thing to particularly look for is if the longer-run forecast for the midpoint of the fed funds target range is lowered from the 2.8 percent in the June forecast. Finally, there may be an indication that the FOMC is seeing conditions for the economy in the next couple that support a change in the pace of rate cuts compared to recent forecasts.

Chair Jerome Powell’s press briefing at 14:30 ET on Wednesday will be a challenge to strike the right tone. His task will be to set market expectations at the start of a rate cut cycle. He will try to reinforce that the fight against allowing inflation to become entrenched is not done and that maximum employment can be maintained through cautious removal of restrictive monetary policy. However, reporters will bring up questions about Fed independence in setting policy at a time of political contention. The Chair will keep to the same line as he has in the past, i.e. the FOMC focuses on the economic data and sets policy accordingly without consideration of who may or may not hold elected office. He will fiercely defend the Fed’s independence.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.