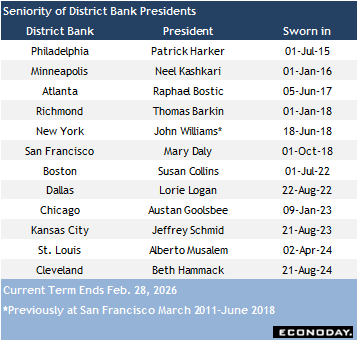

For 2025, the lineup of policymakers that comprise the Federal Open Market Committee (FOMC) looks stable. The normal rotation of voting presidents of the district banks does not include anyone who will be retiring in 2025. Only Philadelphia Fed President Patrick Harker is coming up on mandatory retirement in June 2025. The Philadelphia District does not vote again until 2026.

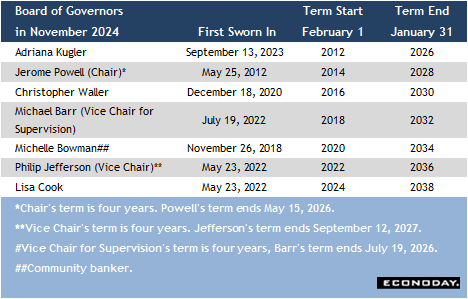

None of the members of the Board of Governors sees an end of term before January 2026. Jerome Powell’s term as Chair runs until mid-May 2026, Philip Jefferson’s term as Vice Chair ends in mid-September 2027, and Michael Barr’s run as Vice Chair for Supervision is until mid-July 2026. There is no mandatory retirement age for the Board of Governors.

Absent an unforeseen event, the FOMC should have the full complement of seven members of the Board of Governors to vote in 2025.

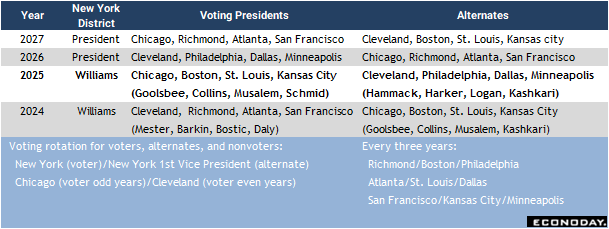

The rotation among district bank presidents as voters takes place at the January 28-29, 2025 FOMC meeting. If for some reason the FOMC would need to vote on a rate action prior to then, it will be the 2024 lineup of voters.

A number of housekeeping items take place at the first FOMC session of the year. This includes appointing in the Chair of the Board of Governors as the Chair of the FOMC and the President of the New York Fed as the Vice Chair of the FOMC. The New York Fed president has a permanent seat among the voters while the four remaining votes for district bank presidents rotate in a fixed order. In 2025, these will be Chicago’s Austan Goolsbee, Boston’s Susan Collins, St. Louis’ Alberto Musalem, and Kansas City’s Schmid). As a group, this are among the less senior of the district bank presidents, especially the latter two. This should not have much implication for the policy outlook. These are likely to be centrist voters in agreement for a carefully managed path of removing monetary policy restriction based on the economic data.

As such, next year’s crop of voters does not suggest any fundamental shifts in the outlook for rates as Fed policymakers try to correctly calibrate rates to achieve the dual mandate of maximum employment and price stability. At the moment, the risks of the labor market deteriorating seem low and progress on getting inflation under control nearly achieved. With the US economy performing well, the prospect of steadily declining rates is good for the short term. However, a new Administration will present new challenges that policymakers will have to navigate when finalized.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.