The FOMC meets on Tuesday and Wednesday in the December 16 week with the FOMC statement and update to the quarterly summary of economic projections (SEP) expected at 14:00 ET on Wednesday. Chair Jerome Powell will follow with his press conference at 14:30 ET on Wednesday.

Markets widely expect a 25-basis point decrease in the fed funds target rate range down to 4.25-4.50 percent after the rate reduction on November 8 that set it at 4.50-4.75 percent. However, recent data reports on inflation and the labor market suggest this is not a done deal.

On the price stability side of the dual mandate, cautious Fed policymakers will mull over whether the stall in disinflation in consumer and producer prices is reason to pause rate cuts. On the side of maximum employment, the one-tenth uptick in the November unemployment rate to 4.2 percent is negligible. An unemployment rate in the low 4’s is consistent with a healthy labor market. While the seasonally adjusted data on initial jobless claims took a sharp turn higher in the December 7 week, this could be the result of the late timing of the Thanksgiving holiday that pushed some layoffs back a week. Labor market conditions may be marginally less tight in November and early December but remain solid for now.

Fed policymakers will be looking at the totality of the data, as Powell has often said. There are two pieces of the data puzzle that will be available before the FOMC finishes its deliberations on Wednesday.

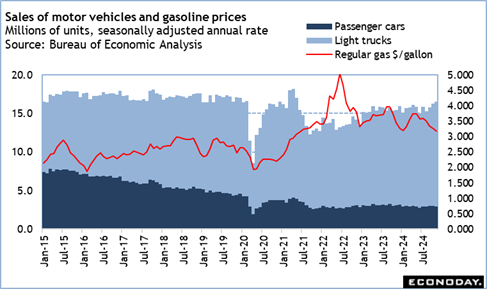

First, the retail sales numbers for November at 8:30 ET on Tuesday will give a solid hint on consumer spending in the third quarter 2024. With Black Friday falling so late in the month, the report may not fully capture spending, although retailers were making a big push to get gift shopping off to an early start before then. There may also have been a boost to sales in early November from spending related to disaster recovery. For example, replacement of motor vehicles was likely one reason behind the increased pace of sales to 16.5 million units at an annual rate in November after 16.3 million units in October and 15.8 million units in September. On the other hand, sales at gasoline stations won’t see higher dollar sales as an increased volume of sales for travel in November while the price per gallon was declining.

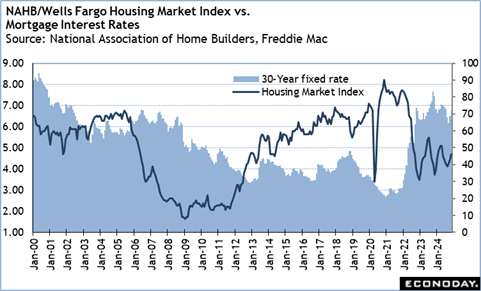

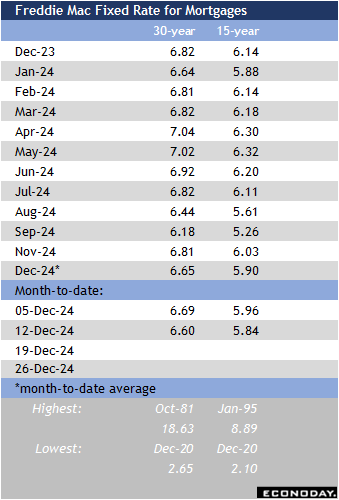

Second, is whether the NAHB/Wells Fargo housing market index shows further firming in early December after a 3-point rise to 46 in November when it is released at 10:00 ET on Tuesday. Recent declines in mortgage rates suggest that buyers will return to the market in hopes of better affordability while inventories are more plentiful, and they have more power to negotiate on prices and terms.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.