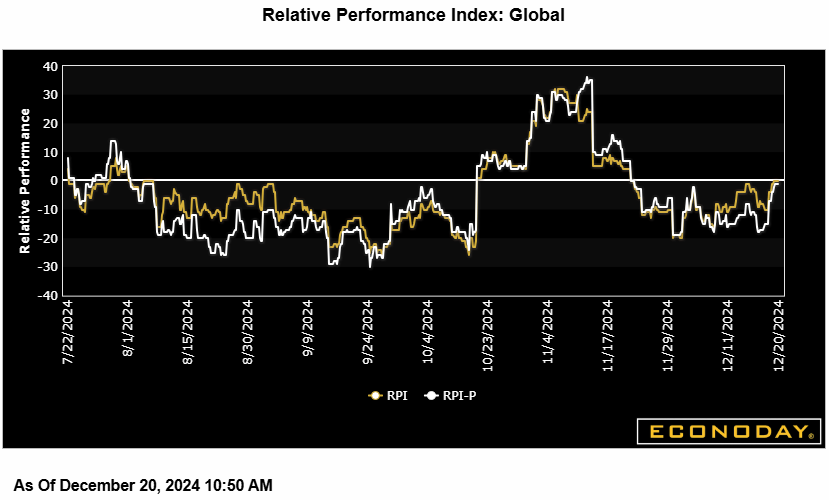

Econoday’s Relative Economic Performance Index (RPI) edged up to exactly zero last week, showing recent global economic activity matching market forecasts. However, within the mix, China continues to underperform alongside Canada and Switzerland and the Eurozone is only just about on track. By contrast, the U.S. is still running marginally hotter than expected and Japan now significantly so.

In the U.S., a very mixed week for data saw the RPI end the period at 8 and the RPI-P at 14. Accordingly, overall economic activity is behaving a little stronger than anticipated, supporting the Federal Reserve’s more cautious attitude towards interest rate cuts in 2025.

In Canada, another downside surprise on inflation in November provided further ammunition to justify the Bank of Canada’s latest 50 basis point ease. It also helped to push the RPI (minus 16) further below zero. With the RPI-P (minus 13) also lower on the week, another, albeit probably less aggressive, cut is likely not too far away.

In the Eurozone, better, albeit far from strong, news on the economy in December helped to lift the RPI to minus 2 and the RPI-P to minus 7. However, even if forecasters are now almost in tune with recent activity, growth is very sluggish and the European Central Bank can be expected to deliver interest rates cuts rather faster than most next year.

In the UK, no change from the Bank of England last Thursday was widely expected. However, following nearly two months of unbroken negative RPI and RPI-P readings, the bank was obliged to downgrade its fourth quarter growth forecast. That said, both measures (RPI at 8 and RPI-P at 9) at least ended the week showing very recent economic activity moving marginally ahead of forecasts.

In Switzerland, inflation gauges continue to surprise on the downside and trimmed the RPI and RPI-P to minus 13 and minus 8 respectively. Sluggish economic activity, weak prices and a strong local currency leave the door wide open to a negative Swiss National Bank policy rate in 2025.

In Japan, the Bank of Japan’s decision to leave policy on hold last week was not expected by some but was nonetheless consistent with a very mixed overall economic performance in recent weeks. Still, with early signs of surprisingly strong December inflation boosting the RPI to 56, market speculation about the next tightening will quickly switch to the central bank’s next meeting in January.

In China, an essentially empty data calendar left both the RPI (minus 21) and RPI-P (minus 30) showing economic activity still undershooting forecasts and investors waiting for a fresh round of monetary easing.

Econoday’s RPI provides a handy summary measure of how an economy has recently been evolving relative to market expectations.

A reading above zero means that the economy in general has been performing more strongly than expected and vice versa for a reading below zero. The closer is the value to the maximum (+100) or minimum (-100) levels, the greater is the degree to which markets have been under- or over-estimating economic activity. A zero outturn would imply that, on average, the market consensus has been correct. Note too that the index is sensitized to place extra weight upon those indicators that investors consider to be the most important.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.