There are three reports in the January 13 week that are likely to stand out, especially in the context of the upcoming FOMC meeting on January 28-29. The numbers available for the labor market through December suggest that the maximum employment side of the Fed’s dual mandate is in good shape. Relatively little layoff activity and tempered hiring is keeping the unemployment rate at levels consistent with healthy conditions able to absorb new workers and provide jobs for those active in the labor market.

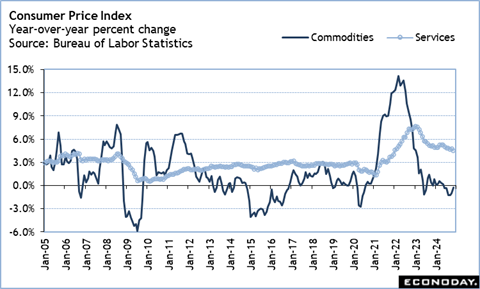

What will be important for Fed policymakers is getting a read on inflation for the price stability side of the dual mandate. The consumer price index (CPI) report is at 8:30 ET on Wednesday. The uptick in the year-over-year increase for the all-items CPI to up 2.7 percent in November came on the heels of a 2.6 percent rise in October that in turn was up two-tenths from the month before. Overall prices have been pushed higher by some short-term factors – like food and gasoline, or insurance premiums. What is more relevant is that the core CPI is stuck at up 3.3 percent year-over-year for the September-November period and has shown virtually no progress since May 2024. The rapid declines in commodities costs that powered disinflation over the past two years are starting to level off while services costs – which have come down significantly in many categories – are slowing the pace of deceleration. A hint that the tempered pace of disinflation is resuming in December would be welcome, but not enough to encourage the FOMC to cut rates again at its January deliberations.

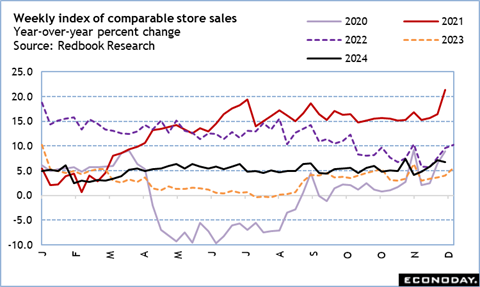

The December numbers on retail and food services sales at 8:30 ET on Thursday could end the fourth quarter 2024 on a solid gain. The Redbook weekly data on sales at comparable stores showed good year-over-year increases as December progressed, suggesting that consumers were in the mood to shop. Online retailers were actively offering deals and advertising heavily to capture some of the holiday spending. Holiday travel probably means an increase in the volume of sales at gasoline stations, as well as more eating out. Higher prices for certain food items – notably poultry and eggs – could mean the higher spending at grocery stores. And a strong year-end for motor vehicle sales should boost the dollar value of spending in that category.

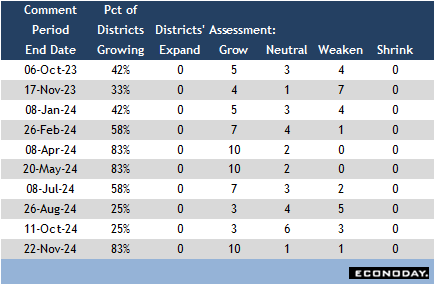

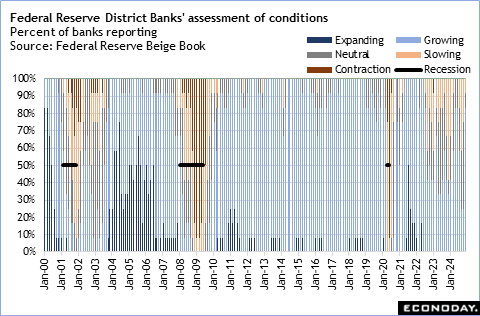

Although not hard data, the Fed’s Beige Book at 14:00 ET on Wednesday is a source of insights that feeds into the FOMC’s consideration of economic conditions across the 12 districts. The anecdotal evidence presented will cover roughly the period between mid-November and early January. It should encompass the initial recovery efforts after Hurricanes Helene and Milton, post-election reactions from businesses and consumers, and the fading prospects of further interest rate cuts by the FOMC. The prior Beige Book released on December 4 indicated that the US economy had moved more decisively back into broad-based growth. This should largely be maintained, but uncertainties about the outlook have grown.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.