Edited by Simisola Fagbola, Econoday Economist

The Economy

Demand

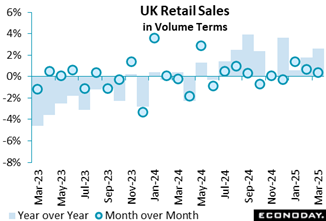

UK retail sales in March 2025 sustained a positive momentum, marking the third consecutive monthly rise with a 0.4 percent increase in volumes, 0.8 percentage points ahead of the consensus forecast. Over the year, retail sales rose 2.6 percent and 0.6 percent ahead of the forecast. This was driven by strong performances in non-food sectors, notably clothing and garden supply stores, which benefited from the UK’s unusually sunny and dry March, the third sunniest on record.

Notably, clothing retailers thrived, bolstered by favourable weather conditions encouraging outdoor activities and purchases. However, the gains were partially undermined by a continued slump in food store sales, particularly in supermarkets, which fell 1.3 percent in March following a 2.2 percent drop in February. Online retail also contributed positively, with a 2.0 percent monthly rise in spending and an increase in the share of total sales from 26.4 percent to 26.8 percent, signalling sustained digital engagement by consumers.

Despite these improvements, total retail volumes remain marginally (0.3 percent) below pre-pandemic levels from February 2020, suggesting that while the sector rebounds, full recovery is still underway.

Housing

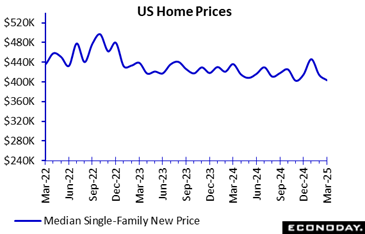

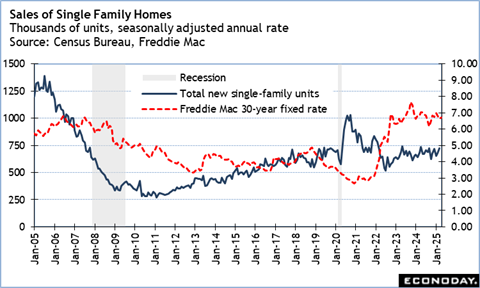

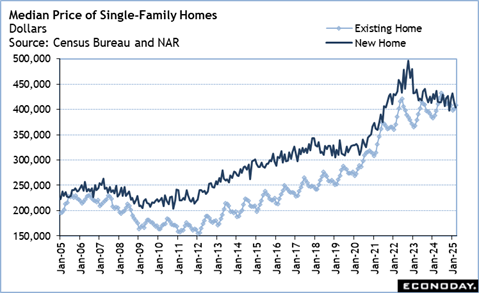

US sales of new single-family homes jump 7.4 percent to a seasonally adjusted annual rate of 724,000, well above the consensus of 682,000 in the Econoday survey of forecasters. Sales are up 6.0 percent from 683,000 in March 2024. The total likely got a boost from a dip in mortgage rates which allowed homebuyers to exercise some pent-up demand. Sales are uneven across regions. Sales are down 1.4 percent in the West and off 22.2 percent in the Northeast – both regions with typically higher home prices. Sales gain 13.6 percent in the South and up 3.0 percent in the in the Midwest. Sales in the South probably follow on destruction of housing stock in October and November 2024. Midwest homes are generally in the more affordable price ranges and benefit from a dip in rates.

The Freddie Mac weekly average rate for a 30-year fixed rate mortgage had a recent peak of 7.04 percent in the January 16 week and has since fallen to a low of 6.63 percent in the March 6 week. Homebuyers who could qualify for a mortgage and ready to buy a home took advantage of the dip in rates. Mortgage rates remained relatively steady until the April 17 week when they jumped 21 basis points to 6.83 percent. The higher level will choke off buying again.

The price of a new single-family home in March is down 1.9 percent to a median $403,600. This suggests that new sales are generally of smaller units in lower price ranges. The supply of homes available for sales is down to 8.3 months’ worth in March. In addition to buyers reducing some inventory, homebuilders are also cutting back on starting homes in the face of less demand.

The share of total sales going to homes not yet started is 11 percent in March, well below hot housing market in late 2020 and early 2021 when units not started saw a peak at 35% in November 2020. Units under construction have a 36 percent share of sales. The majority of buyers are opting for finished units.

Sentiment

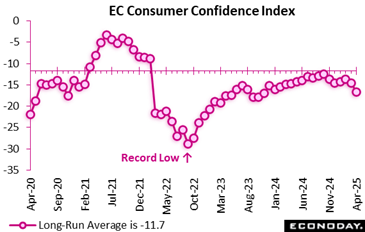

The April 2025 Eurozone consumer confidence index reveals a sharp downturn in consumer sentiment across the euro area. The confidence indicator fell by 2.2 percentage points to minus 16.7, about 1.6 points below the consensus forecast for the month.

This update marks the second consecutive monthly decline and the lowest confidence level in 18 months. The drop signals growing consumer pessimism, likely reflecting concerns over geopolitical uncertainties and trade uncertainties from the US. More worryingly, confidence now stands well below its long-term average, suggesting a broader erosion of trust in the economic outlook.

If this trend continues, it could dampen household spending, slow economic recovery, and challenge the European Central Bank’s policy goals.

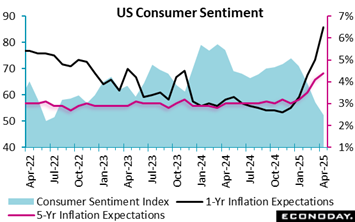

US consumer sentiment was not as disastrously bad in the final April reading as in the preliminary report but it remained down a remarkable 8 percent from March. The sentiment index came in at 52.2 in the final April report versus 50.8 in the preliminary April figure and 57.0 in the March final. The Econoday consensus looked for 50.5 for the final April index.

One-year inflation expectations came in at a horrifying 6.5 percent in the final April report versus 6.7 percent in the preliminary April, and versus what now seems like a moderate 5.0 percent in March. That is up from 4.3 percent in February and 3.3 percent in January. The University of Michigan said inflation fears seemed to diminish a bit after President Trump’s April 9 partial “pause” in his universal tariffs unveiled on April 2.

The report cited consumer worries about tariffs and rising inflation as the primary reason for falling sentiment. Views of current conditions are down but relatively stable compared with expectations that have fallen out of bed, down 32 percent since January. This is the steepest three-month percentage decline seen since the 1990 recession. Consumers are increasingly bearish on expectations for their personal finances and business conditions.

Business Surveys

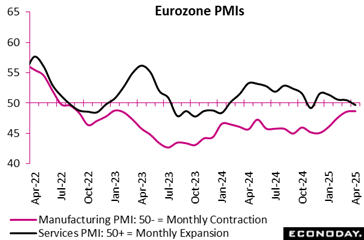

Eurozone business activity stagnated in April 2025, with the composite PMI barely above contraction at 50.1—a four-month low—reflecting deepening uncertainty and a steep decline in new orders, the sharpest this year. Services slipped into contraction (49.7), while manufacturing showed slight but improving resilience (48.7), marking its highest reading in over two years.

Business confidence has fallen since late 2022, with firms across all major economies growing cautious about future prospects. Demand remains weak, dragged down by shrinking export orders—an uninterrupted trend since March 2022. France continued to decline, Germany reversed its March growth, and only the rest of the bloc maintained modest output expansion.

Employment gains from March evaporated, as staff cuts in manufacturing offset slight service sector hiring. Despite minimal job creation, firms effectively worked through existing backlogs, signalling little pressure on capacity.

Inflationary pressures cooled across the board, with input costs rising more slowly, especially in manufacturing, where costs declined. Nonetheless, output charges increased, particularly in manufacturing, which saw its fastest inflation in two years. Meanwhile, supply chains improved further, with the fastest delivery times recorded since June 2024.

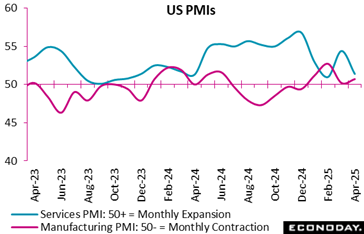

The expected hit from tariffs was less than anticipated in the S&P PMI manufacturing index, which actually edged up to 50.7 in the April flash, a two-month high, from 50.2 in the March final. The Econoday consensus saw the index slipping into modest contraction at 49.4 for the April flash.

The flash services PMI remained positive at 51.4, a two-month low, versus 54.4 in March, and versus the expected 52.5. The composite eased to 51.2 in the April flash, a 16-month low, from 53.5.

S&P said the survey showed 1-year expectations fell to one of the lowest levels since the pandemic. Prices received for goods and services rose at the fastest pace for a year, with “an especially steep increase reported for manufactured goods, linked to tariffs.”

US Review

What’s Up with Home Sales?

By Theresa Sheehan, Econoday Economist

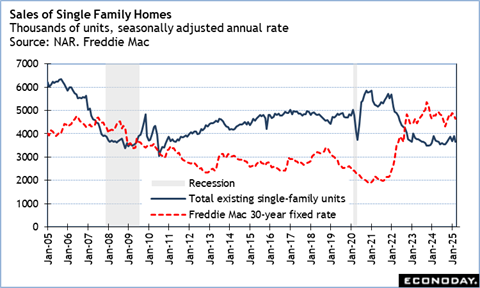

There’s an apparent contradiction in the March data on sales of single-family homes. Sales of new single-family homes in March rose 7.4 percent to a seasonally adjusted annual rate of 724,000 units. Sales of existing single-family homes decline 6.4 percent to 3.64 million units in March.

The difference is easily explained by movements in mortgage rates since the start of the year. New home sales are counted in the month in which the sales contract is signed. Existing home sales are counted when the buyer and seller successfully close the deal.

March sales of new homes are using mortgages obtained more recently – when rates have dipped. March sales of existing homes were completed with mortgages taken out a month or two earlier.

The consistent influence on sales is mortgage rates. There was an opportunity to take out a home loan at a more favorable rate in February and March. The Freddie Mac weekly average for a 30-year fixed rate loan was at a recent peak of 7.04 percent in the January 16 week, but fell steadily there after to 6.63 percent in the March 6 week. It then inched a bit higher in subsequent weeks, then bottomed at 6.62 percent in the April 10 week. Rates at those levels are done for the time being. The average 30-year fixed rate jumped 21 basis points to 6.83 percent in the April 17 week. Mortgage rates approaching 7 percent tend to cool homebuying. In the present uncertain economic environment, there will likely be moderation in home buying in the coming months.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.