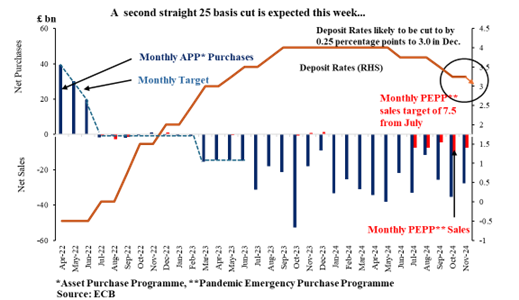

The European Central Bank (ECB) is anticipated to cut its key deposit rate by 0.25 percentage points at Thursday’s announcement, bringing the rate to 3.00 percent. This aligns with the ECB’s broader strategy to achieve its 2 percent inflation target amidst weakening economic growth in the Eurozone. Current inflation stands at 2.3 percent, marginally above the target, yet analysts suggest that inflationary pressures are under control due to recent stabilisation. We expect a continued trajectory of rate cuts into 2025, potentially bringing the deposit rate to 2 percent or lower. While the ECB is likely to maintain a data-dependent, meeting-by-meeting approach without forward guidance, this strategy allows for flexibility in addressing economic uncertainties.

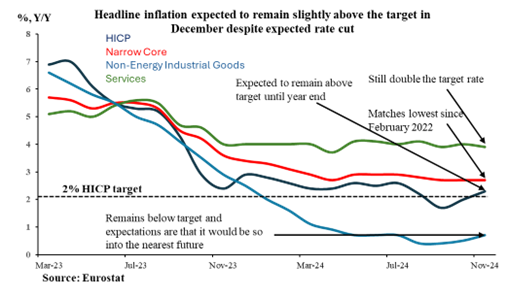

The likelihood of a cut this week is high even though the November flash HICP report showed headline inflation climbing to 2.3 percent. More importantly, the core rates were also well behaved and at 2.7 percent, the narrowest gauge matched its lowest mark since January 2022. Despite service inflation remaining double the target, considered temporary, this remains a concern as the ECB remains committed to easing monetary policy to support economic activity, underscoring the ECB’s proactive approach to achieving its policy objectives. While lingering effects from the Paris Olympics may have contributed to the elevated inflation rate, the broader trend in services inflation has remained almost flat as it dropped to 3.9 percent from 4.0 percent. This persistent “stickiness” in prices can fuel resistance from policymakers hesitant to approve another interest rate cut before the ECB presents its updated inflation forecast, scheduled for December.

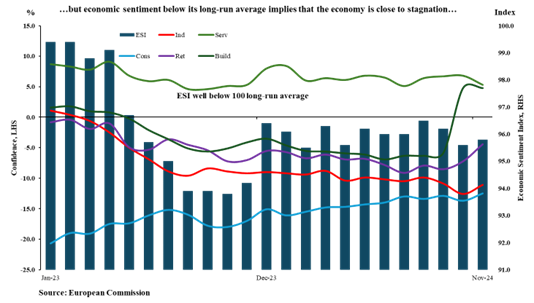

That said, subdued, and probably slowing, economic activity is adding to pressure for lower borrowing costs. The ECB trimmed its growth forecast at the last meeting but with the latest business surveys showing still subdued confidence, it may well have to do so again. Firms face weak demand at home and abroad, ensuring that the European Commission’s economic sentiment index, a measure watched closely by the ECB, remains well below its 100 long-run average. To be sure, current levels point to stagnation rather than expansion. Similarly, retail sales have gone nowhere since the end of last year and, at 48.1 in November, S&P Global’s composite PMI is back below the 50-expansion threshold, an occurrence over the last three months. Regionally performances have been mixed and the Spanish economy for one has actually done well. However, as for the two largest states, Germany’s leading economic institutes are no longer forecasting any growth at all this year and in France, INSEE now expect GDP to shrink 0.1 percent this quarter.

In fact, economic activity in general has generally fallen short of market expectations despite witnessing a slight surge in late October and early November as well as seeing a slight uptick in early December, since the September discussions. Econoday’s relative performance index (RPI) has spent most of the period in negative surprise territory, averaging minus 15, a value a few points below the measure excluding inflation shocks (RPI-P) which averaged minus 12. In other words, the broader picture is one of a disappointingly soft economy that could do well with some central bank stimulus.

The ECB’s rate cuts aim to address downside risks to the eurozone economy, including potential US trade restrictions and ongoing political instability. Trade tariffs anticipated in 2025 are a significant concern, with potential impacts on export-dependent industries. In addition, political instability in France and Germany has created further economic headwinds. France’s government crisis has widened bond spreads, signalling heightened country-specific risk, while Germany faces fiscal policy challenges due to coalition disagreements over its “debt brake.”

From a market perspective, rate cuts are expected to bolster equity markets, as lower rates reduce borrowing costs and stimulate economic activity. In bond markets, falling rates typically push bond prices higher due to lower yields. However, savers may face reduced returns on deposits, while borrowers benefit from cheaper financing options for consumer debt and mortgages.

In essence, the ECB’s current monetary policy trajectory underscores its determination to bring inflation back to target without adding unnecessary recession risks. While the focus remains on controlling inflation and stimulating growth, risks from geopolitical tensions and domestic political instability could shape future policy adjustments. Markets are poised to respond positively to rate cuts, though the balance between stimulating growth and managing inflationary risks will be crucial.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.