The economic picture facing the SNB as it prepares for December’s Monetary Policy Assessment (MPA) is little changed from that at the time of the September report. Indeed, inflation has fallen even further and is threatening to slide back below zero, the domestic economy remains sluggish and an already uncomfortably strong Swiss franc has continued to appreciate. Just a few weeks ago, the SNB was insisting that additional interest rate cuts should not be taken for granted. However, by late last month, Chairman Martin Schlegel was warning that negative rates might be required to prevent the Swiss currency gaining yet more ground. Consequently, not only are forecasters confident that Thursday’s announcement will include a fourth successive reduction in the policy rate, but a significant minority now favour a 50 basis point move over the consensus 25 basis point cut to 0.75 percent. The latter level would match the lowest level since December 2022.

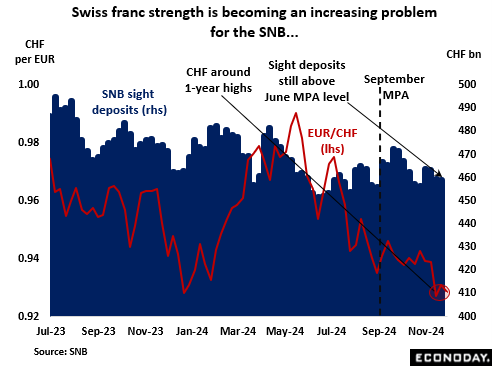

Amid rising geopolitical tensions, the franc continues to demonstrate its status as Europe’s premier safe haven currency. Since the middle of July, the Swiss unit has risen around 5 percent versus the euro and is currently trading around a 1-year high. The SNB has previously intimated that it was happy to see the cross-rate stabilise around CHF0.95 but for the last three months, the franc has consistently been on the strong side of that mark. The persistent overshoot warns that without a cut in key rates, competitiveness losses could well become all the more acute. Indeed, concerns about the buoyancy of the local unit have effectively prevented the central bank from making any further inroads into its balance sheet. At CHF835.2 billion in October, total assets were nearly CHF30 billion more than in August.

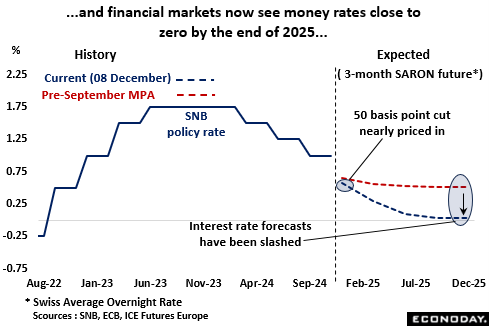

Financial markets believe the central bank has little choice but to ease again. A 50 basis point cut is almost fully priced in for this week and expectations for 2025 have been revised down significantly. In fact, by the end of next year, 3-month money rates are now seen just a few basis points above zero. And while the SNB is known not to be a fan of negative interest rates, the bank has made it very clear that it is prepared to go down that route should its price stability goals come under threat.

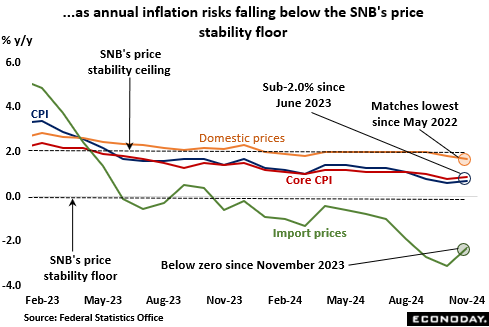

There has been little in the recent data to suggest any diminution in deflationary pressures. Headline CPI inflation was running at an annual 0.7 percent rate in November, its third straight month below 1 percent and well on course to undershoot the central bank’s 1 percent fourth quarter forecast. Moreover, the core measure was not much higher at just 0.9 percent. Both gauges are dangerously close to the bottom end of the SNB’s definition of price stability, inevitably raising the risk that inflation could soon go negative for the first time since early 2021. Not helping matters is the buoyancy of the local currency which has been a key factor weighing on import price inflation which has now been below zero for a full year.

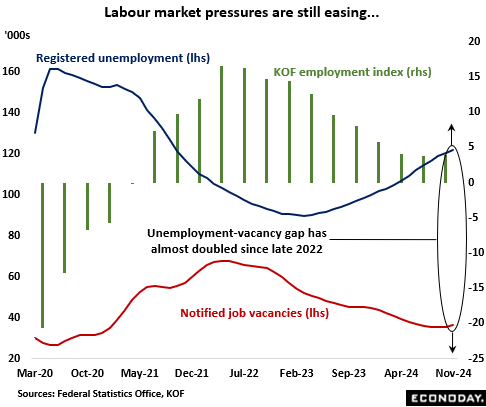

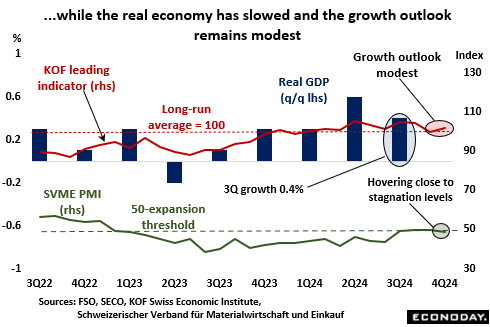

Meantime, the labour market has continued to loosen, albeit still only gradually. Since the September MPA, unemployment has risen a further 5,000 or more than 4 percent, and, at 2.6 percent, the November jobless rate matches its highest reading since September 2021. More promisingly, vacancies have recently shown signs of stabilising but last month were still nearly 18 percent lower on the year and their shortfall versus the number of people unemployed is close to 3-year highs. Moreover, while the KOF’s October employment survey found private sector businesses on average expecting to add to headcount over the coming three months, the rate was little changed from the 3-year low posted in July.

Economic growth was a respectable 0.4 percent in the third quarter. However, this was down from 0.6 percent in April-June and although domestic demand contributed fully 2 percentage points, 1.8 percentage points of that came from inventory accumulation. In addition, gross fixed capital formation contracted for a third time in the last four quarters. In any event, the SNB will note another ominously weak performance by goods exports which fell 3.9 percent following a 6.5 percent slump in the second quarter. This made for a hefty cumulative 5.5 percentage point hit on growth and will have exacerbated the central bank’s concerns about competitiveness losses caused by the strength of the franc. Leading indicators point to at best only a modest rate of expansion over coming months which, if correct, is unlikely to significantly impact the current soft inflation trend.

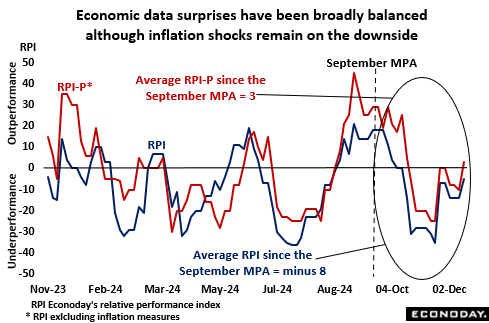

Since the September MPA, downside surprises in the data have been slightly more prevalent than upside shocks, reflected in Econoday’s Relative Economic Performance Index (RPI) averaging minus 8 over the period. Still, an RPI-P of 3 shows that real economic activity has been evolving much as expected, the difference between the two gauges showing forecasters still underestimating the speed at which inflation has fallen. Such a mix also strengthens the case for additional monetary stimulus.

Against this backdrop, a further step towards a negative policy rate would appear all but inevitable, especially since the ECB also looks poised to ease this week. The SNB is known for its willingness to surprise financial markets but the main question mark over this Thursday’s announcement is just the size of the cut.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.