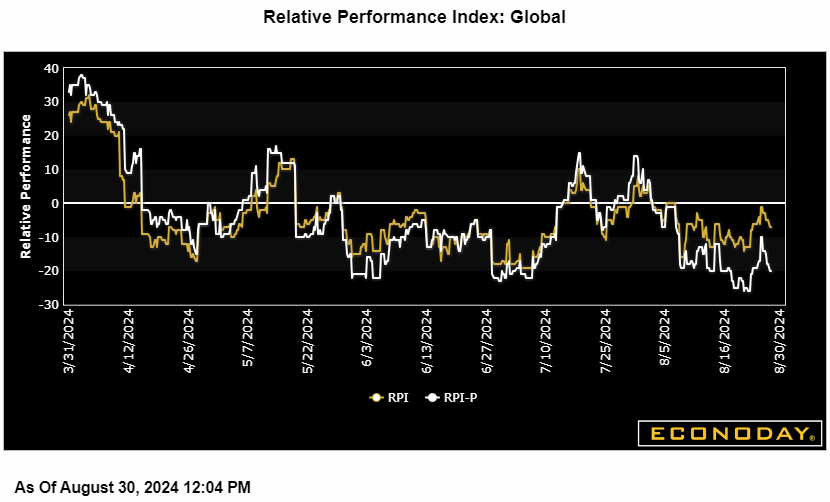

Global economic data continue to underperform expectations, at minus 10 on Econoday’s Relative Performance Index and at minus 21 when excluding price data (RPI-P). The latter offers an indication on real economic activity which has been subpar for nearly the whole of August.

But the Eurozone is outperforming and financial markets remain confident that the European Central Bank will cut key interest rates at its September 12 meeting. However, still sticky core and services inflation along with a new record low jobless rate helped lift the region’s RPI and RPI-P to 14 and 22 respectively in strength that suggests there is still room for disappointment, that the ECB may not cut after all.

Canada is also outperforming, going into the week at 37 and 42 on the RPI readings and slowed down only slightly by the mixed GDP data, to 32 overall and 35 for the RPI-P. These are still very solid readings that won’t be increasing pressure on the Bank of Canada to further cut rates at its Wednesday, September 4 meeting.

In the UK, a majority of downside surprises ensured that both the RPI (minus 19) and RPI-P (minus 14) remained below zero. Both readings will help to support speculation about a possible second straight ease by the Bank of England at its September 19 meeting, but the decision is likely to be very close again.

In Switzerland, more than two months of marked economic underperformance ended as the RPI climbed to minus 1 and the RPI-P to exactly zero. Even so, the latest data show activity only matching what have been modest market expectations and keep alive the chances of a third successive cut in the Swiss National Bank’s policy rate on September 26.

In Japan, the latest data point to moderate growth and higher inflation. However, surprises were still biased to the downside and reduced the RPI to minus 26 and the RPI-P to minus 57. Such readings will not add to pressure on the Bank of Japan to tighten again even though the medium-term outlook for interest rates is still up.

The US entered the week with a slight upward bias at plus 13 for both readings but ended the week with a slight downward bias, at minus 7 and minus 11. Though there is still the August employment report and the August CPI still to go before the Federal Reserve’s September 18 announcement, a rate cut has been conclusively signaled.