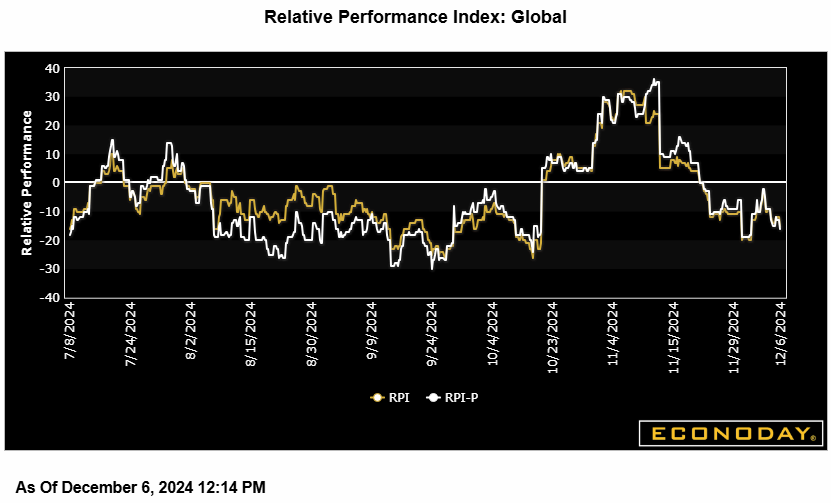

Econoday’s Relative Economic Performance Index (RPI) slipped further below zero last week. At minus 16, the latest reading shows recent global activity struggling to keep up with market forecasts. The U.S. and Canada are essentially matching expectations but China, the Eurozone, Japan, and the UK are all falling short.

In the U.S., the key November employment update helped to lift both the RPI and the RPI-P to 2. In other words, economic activity in general is performing much as anticipated which should leave forecasters all the more confident about another 25 basis point cut by the Federal Reserve next week.

In Canada, a mixed November employment left the RPI at exactly zero and the RPI at minus 8. Overall, recent data have contained few surprises and will have done nothing to dent expectations for another cut in Bank of Canada interest rates on Wednesday.

Ahead of Thursday’s European Central Bank announcement, the Eurozone RPI and the RPI-P closed out the week at minus 15 and minus 12 respectively. Neither reading indicates forecasters being especially wide of the mark but underperformance has been a feature of the economy since mid-November. A 25 basis point cut still looks the best bet with a not insignificant chance of 50 basis points.

In the UK, downside surprises continue to dominate and put the RPI at minus 11 and the RPI-P at minus 35. Consistently sub-zero readings since late October have kept the door open for another cut in Bank Rate next week but the unexpectedly firm October inflation update still makes a steady stance more likely.

In Switzerland, a firmer than expected November labour market helped to nudge the RPI (minus 5) to within striking distance of zero. Accordingly, with the RPI-P (3) even closer, the message is that recent economic activity in general has all but matched forecasts. However, that still leaves the Swiss National Bank on course to announce at least a 25 basis point cut on Thursday and, quite probably, a larger 50 basis point ease.

In Japan, surprisingly strong household spending was only enough to lift the RPI to minus 14 and the RPI-P to minus 35. Downside shocks still hold the balance but accelerating inflation will keep the Bank of Japan in tightening mode, albeit at probably only a modest pace.

In China, early indications of surprisingly sluggish activity in November dragged the RPI down to minus 36 and the RPI-P to minus 33. The impact of the recent massive wave of stimulus measures is not currently living up to expectations.

Econoday’s RPI provides a handy summary measure of how an economy has recently been evolving relative to market expectations.

A reading above zero means that the economy in general has been performing more strongly than expected and vice versa for a reading below zero. The closer is the value to the maximum (+100) or minimum (-100) levels, the greater is the degree to which markets have been under- or over-estimating economic activity. A zero outturn would imply that, on average, the market consensus has been correct. Note too that the index is sensitized to place extra weight upon those indicators that investors consider to be the most important.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.