With Christmas, Hanukkah, and other holiday observances dominating the calendar for the next two weeks, there is very little on the US economic data schedule that will demand attention. Most of the numbers will put the final touches on perceptions of economic conditions as the fourth quarter 2024 draws to a close. Most notable will be the remaining numbers related to the housing market in November and conditions in manufacturing in December.

Pivotal to interpreting the November housing data will be the FOMC decision and forecast released on December 18. While the FOMC lowered short-term rates by 25 basis points, its collective forecast indicated that rate cuts would be fewer in 2025. An economy that continues to expand at a higher pace than forecast, a labor market that has cooled but not gone cold, and inflation that is slow to exit as expressed in the measures of upward price pressure means Fed policymakers can take their time in easing restrictive monetary policy. Fed Chair Jerome Powell has called the current fed funds target rate of 4.25-4.50 percent “meaningfully” restrictive while at the same time the rate has been cut a significant 100 basis points from its recent peak.

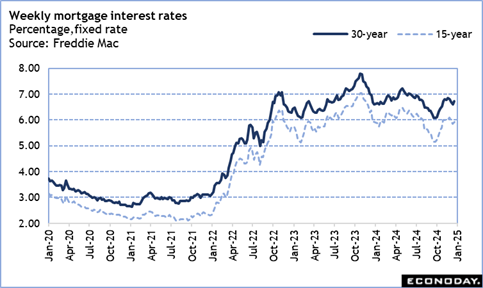

The impact on financial markets is that long-term rates – notably mortgage rates – are going to remain higher for the time being. This will affect lending and borrowing decisions in terms of creditworthiness versus willingness to borrow at current rates. Consumers and businesses will be more likely to make decisions based on necessity rather than less demanding criteria.

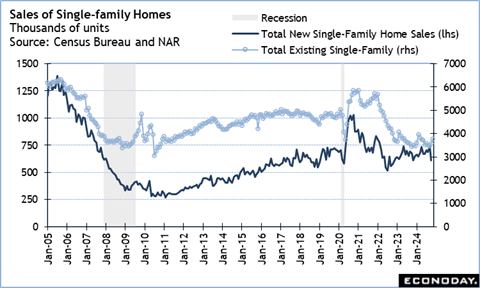

While sales of existing single-family homes came in at solid 3.76 million units in November at a seasonally adjusted annual rate, sales of new single-family homes may not keep pace. November existing home sales benefited from increased supply and a dip in mortgage rates in September and the motivation of rising mortgage rates in October to get contracts signed in those months and closed in November. New home sales are for contracts signed in November when the rate was going up again. The Freddie Mac rate for a 30-year fixed rate mortgage had a monthly average of 6.18 percent in September, rising to 6.51 percent in October and 6.81 percent in November. Rates moderated a bit in early December but that reversed after the FOMC decision.

The NAR pending home sales index for November is going to also be an interest rate story where homebuyers who locked in a lower rate in October signed contracts before rate locks expired. This probably means home resales will be solid for December. January may be a different story.

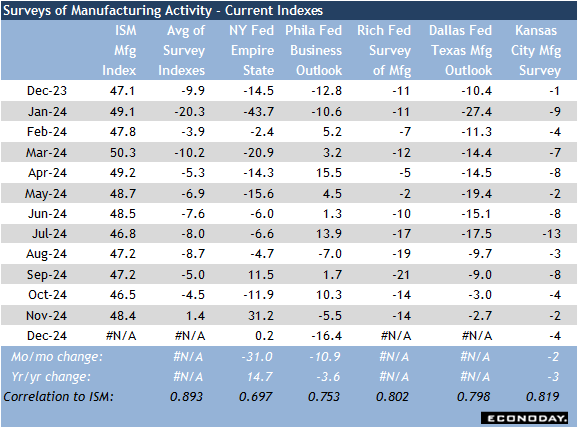

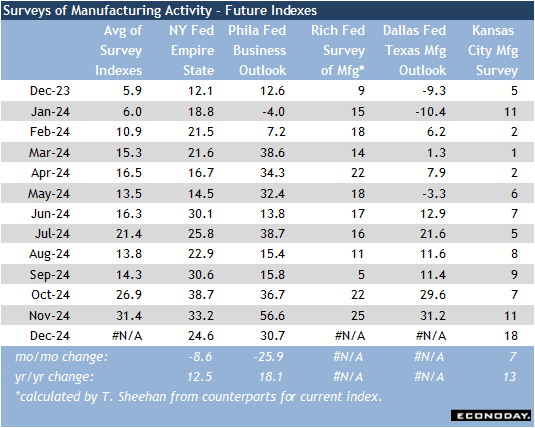

Three of the five Fed district bank surveys of manufacturing in December have been published – New York, Philadelphia, and Kansas City. The Richmond Fed manufacturing composite index is set for release at 10:00 ET on Tuesday, December 24 and the Dallas general activity index is at 10:30 ET on Monday December 30. So far it looks like December will end the year on a down note for the factor sector while expectations for six months from now are generally more cautious, if for moderate activity.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.