The New Year’s Day observance sits in the middle of the December 30 week. This means some disruptions to normal release patterns. There is an early close for bond markets on Tuesday, and a full close for both stocks and bonds on Wednesday.

The data release calendar is light and does not include a lot of market moving potential. There will be private industry reports about the health of retail sales over the holiday period. So far it seems that shoppers were willing to spend if they found bargains and they were also conscious of the possibility that some consumer goods will be costlier in the near future and/or in shorter supply. Some planned spending may have occurred in the fourth quarter 2024 that is borrowed from the first quarter 2025.

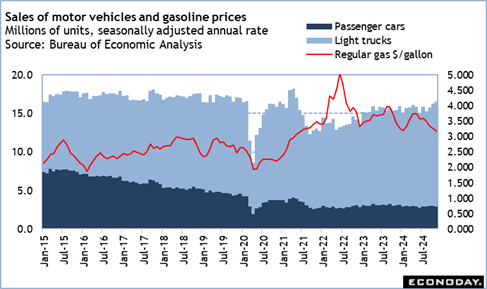

One bellwether could the numbers on new motor vehicle sales for December which are expected on Friday. There was an uptick in the seasonally adjusted annual pace of sales to 16.5 million units in November. However, some of that could have been related to replacing vehicles lost to storm damage in late September and early October. In question is how much consumers pulled back from that pace and if the year-end number is above the 15.9 million units at the end of 2023.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.