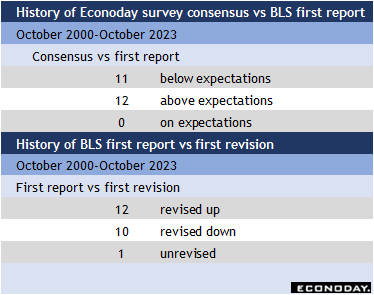

There is nothing on the week’s data calendar that will distract from two big events.

First, the US presidential election will be held on Tuesday, November 5. Most predictions are for a close race that might not be completely settled until after localities count their absentee and provisional ballots. This could take several days. That won’t stop news outlets and/or campaigns from declaring a winner, or at least a likely winner.

Second, the FOMC meets on Wednesday and Thursday to deliberate on US monetary policy. Proximity to the election will tinge perceptions of whatever decision is released at 14:00 ET on Thursday. Chair Jerome Powell’s press briefing at 14:30 ET on Thursday may be an exercise in defending the independence of the central bank and its officials’ determination to set politically unbiased policy according to the available data and information. It is probable that Powell will get questions about his future as Chair of the Fed which he will gracefully brush aside as inappropriate to talk about.

The FOMC is highly unlikely to deliver another 50-basis point cut like it did on September 18. Expectations are widely for a 25-basis point cut to bring the fed funds target rate down a notch from the present 4.75-5.00 percent range.

On the maximum employment side of the Fed’s dual mandate, the October employment report will muddy the outlook. The downside surprise of payrolls up 12,000 in October compared to the median market forecast of about 125,000 was a shock on the face of it. However, other reports on payrolls and layoff activity suggest that the headline is more due to special factors than a sudden deceleration in hiring. The fact that the unemployment rate remained at 4.1 percent and that the participation rate was down a tenth to 62.6 percent should be convincing evidence that the underlying conditions are healthy.

On the price stability side, the Fed’s preferred measure of inflation is the PCE deflator. As of September, the overall PCE deflator shows prices up 2.1 percent year-over-year. While that looks great and might be a reason to declare victory in this inflationary episode, the core PCE deflator is up 2.7 percent in September and has been essentially the same since May. The PCE deflator for goods-only is down 1.2 percent year-over-year in September while services prices are up 3.7 percent compared to a year ago. In services, housing and utilities costs are up 4.9 percent from September 2023. This makes it difficult to pronounce inflation has been tamed.

Inflation expectations for the medium term remain above the 2 percent target, but are otherwise well-anchored.

Taken together, in an economy experiencing moderate growth, there is room to cut rates a little more, but no urgency. With the US economy continuing to expand above the Fed’s longer-run forecast of up 1.8 percent, making the case that adding in some stimulus via easier monetary policy is the right move could be tougher, the October payroll headline notwithstanding. There won’t be an update to the FOMC’s quarterly summary of economic projections at the November 6-7 meeting. It will be up to the meeting statement and Powell’s briefing to signal the next steps ahead. One thing is sure to be emphasized, that policymakers are data-dependent and that decisions will be on a meeting-by-meeting basis.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.