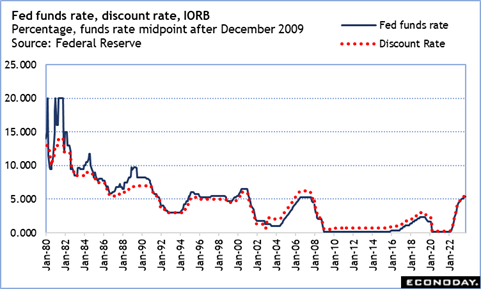

The big question in the October 30 week is whether the FOMC will hold the fed funds target rate range at 5.25-5.50 percent for the second meeting in a row. The present crop of economic data and anecdotal evidence is expected to result in no change in rates after the October 31-November 1 meeting. A resilient US economy grew 4.9 percent in the third quarter. If the labor market reflects slower hiring activity, it also shows few signs of an acceleration in layoffs. Inflation was less improved in the September reports, but at least some of that is due to rising gasoline costs which are now moderating quickly. Tightening in financial markets is doing some of the FOMC’s work in making credit conditions more restrictive. Last week Fed Chair Jerome Powell noted that he thinks there are “meaningful” impacts from past rate hikes still to manifest in the data.

This sets the stage to extend the pause in the current rate hike cycle. However, Fed policymakers will remain hawkish on the inflation outlook and prepared to raise rates further if the data do not indicate further progress in disinflation.

The October employment report won’t be available to the FOMC at the time of the meeting, so policymakers will have to do without any guidance it might or might not provide. October will almost certainly be well below the 336,000 increase in nonfarm payrolls in the September report. Very early estimates for October are running roughly around 150,000 at this writing. This would be a healthy gain for an economy in modest to moderate expansion and consistent with the tone of other labor market reports. Firms are more cautious about hiring at the moment, but they are also taking on experienced workers where they can find them. Service businesses are hiring not only to fill seasonal work but to increase permanent staffing. Goods producers, where sentiment is improving, are trying to retain or find employees with the skills they need. Ongoing strikes could cloud the data in the manufacturing and entertainment sectors.