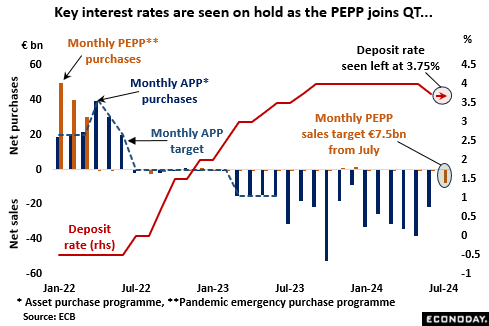

Having delivered the widely anticipated 25 basis point cut in key interest rates in June, the ECB is expected to leave policy unchanged at what will be its last meeting before the summer recess. Since the last gathering, inflation developments have been mixed and the euro has been volatile in the face of diminished easing speculation in the U.S. and the fallout from surprisingly sharp swings to the right and then left in the recent snap French National Assembly elections. Accordingly, Thursday’s announcement is seen holding the key deposit rate at 3.75 percent, the refi rate at 4.25 percent and the rate on the marginal lending facility at 4.50 percent. The bank is also likely to repeat June’s limited forward guidance which stated that it “will keep policy rates sufficiently restrictive for as long as necessary” to achieve the inflation target.

Meantime, balance sheet management became more aggressive at the start of the month as QT was expanded to incorporate the €1.7 trillion pandemic emergency purchase programme (PEPP). As indicated some time ago, the PEPP will face an average monthly target for disposals of €7.5 billion through December whereupon the parameters for next year will be decided upon. With monthly disposals under the longstanding Asset Purchase Programme (APP) averaging around €33 billion so far in 2024, the addition of PEPP sales will be significant.

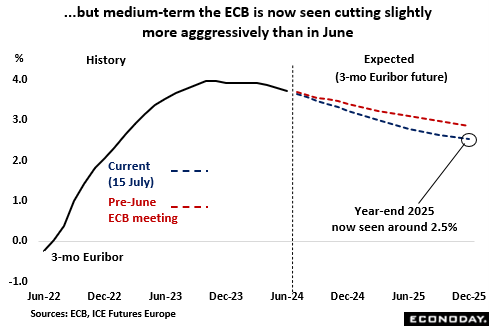

However, financial markets have become more optimistic about how far, and how quickly, interest rates will be lowered over the medium-term. At 3.25 percent, 3-month money rates in December are now expected to be about 15 basis points below the level priced in just before the June meeting. By the end of 2025, rates are seen down an extra 30 basis points at just over 2.5 percent.

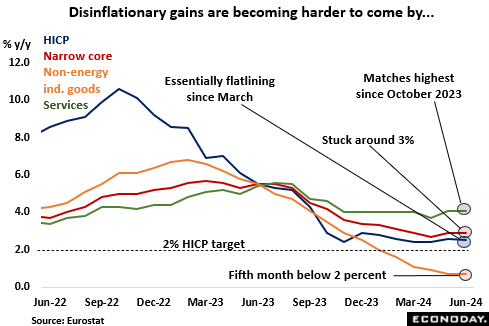

A second successive cut in key rates this week would almost certainly have required a more favourable June inflation report. As it is, although the headline yearly rate dipped a tick to 2.5 percent, it failed to reverse all of May’s bounce and left an essentially flat trend. More importantly, progress on reducing core inflation has also dried up with the narrow underlying rate holding just below 3 percent since March. The stickiness of prices in services, where June’s 4.1 percent post matched the highest since last October, remains a major issue.

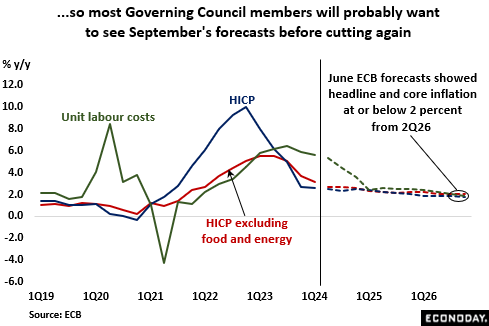

Consequently, the majority on the Governing Council (GC) will probably want fresh reassurance that inflation is still on track to meet its target on a sustainable basis – and that will require an updated set of economic forecasts. The June ease was facilitated by the then new projections that showed headline and core inflation either below 2 percent or on target from the second quarter of 2026. However, those predictions relied heavily upon an assumed marked deceleration in unit labour cost growth which, as the ECB itself concedes, is far from certain. Results of the next forecasting round will not be available until the September gathering.

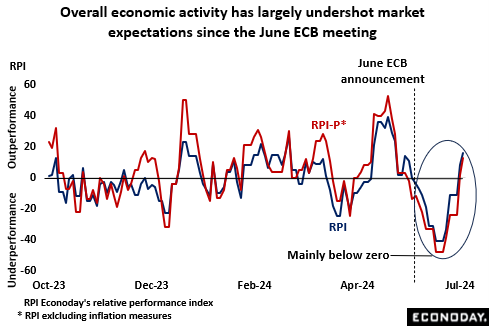

By and large, overall economic activity has been disappointingly soft since the June announcement. Although Econoday’s relative performance index (RPI) currently stands at 16 and, after excluding inflation indicators (RPI-P), at 13, both measures have been in negative surprise territory over much of the period. Indeed, the former averages minus 19 and the latter minus 27, signalling a clear gap between actual developments and market forecasts. With QT being stepped up, such underperformance may prompt some of the more dovish GC members to push for another cut in rates but they are likely to be only a small minority.

In summary, as much as the ECB would almost certainly like to ease again, it will be more determined to avoid the embarrassment of cutting rates too soon only to have to hike them shortly afterwards. As such, confidence that inflation is behaving itself is vital which ought to ensure that policy rates remain on hold until at least September.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.