Edited by Simisola Fagbola, Econoday Economist

The Economy

Monetary policy

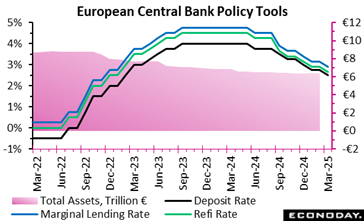

The European Central Bank has delivered another interest rate cut in 2025, lowering all three key rates by 25 basis points. The decision reflects confidence in the disinflation process, with headline inflation projected to ease to 2.3 percent in 2025 before aligning with the 2 percent target in 2026 and 2027. However, rising energy prices and lingering wage adjustments remain inflationary risks.

While the cut aims to stimulate borrowing and investment, the economy still faces headwinds. Growth projections have been revised downward, with GDP now expected to expand by 0.9 percent in 2025, amid weak exports and investment uncertainty. Although rising real incomes and fading rate hike effects could eventually boost demand, subdued lending activity remains a constraint.

The Governing Council is cautious, stressing a data-dependent, meeting-by-meeting approach to future decisions. With no commitment to a specific rate path, the ECB balances easing financial conditions while ensuring that inflation settles sustainably at 2 percent. Meanwhile, the APP and PEPP portfolios continue to decline predictably, reinforcing a gradual unwinding of pandemic-era stimulus.

Inflation

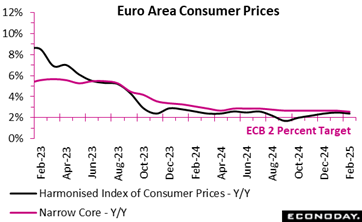

The euro area’s annual inflation rate edged down to 2.4 percent in February, marking a marginal cooling from January’s 2.5 percent. While the decline suggests progress towards price stability, inflationary pressures remain uneven across sectors, highlighting the complexity of the disinflation process.

Services inflation, the most significant contributor to overall inflation, dipped slightly to 3.7 percent from 3.9 percent, reflecting resilient demand but some moderation in cost pressures. However, food, alcohol, and tobacco inflation rose 2.7 percent from 2.3 percent, likely driven by volatile commodity prices and supply chain fluctuations. The most striking shift was in energy inflation, which plunged to 0.2 percent from 1.9 percent, suggesting a sharp cooling of energy costs—a crucial relief for consumers and businesses alike. Meanwhile, non-energy industrial goods inflation ticked up marginally to 0.6 percent, indicating continued but weak pricing power in the manufacturing sector.

Regionally, headline inflation remained stable in Germany (2.8 percent after 2.8 percent), Spain (2.9 percent after 2.9 percent), and Italy (1.7 percent after 1.7 percent), while it fell in France (0.9 percent after 1.8 percent).

Although headline inflation moves in the right direction, core inflation remains sticky, particularly in services and essential goods. This signals that while monetary tightening has had some effect, inflationary risks persist, keeping policy vigilance necessary in the months ahead.

Employment

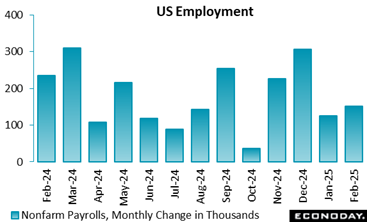

Nonfarm payrolls are up 151,000 in February, not materially different from the consensus of up 160,000 in the Econoday survey of forecasters. There is a minimal net revision of down 2,000 to the prior two months. The unemployment rate is a tenth higher at 4.1 percent in February, just above the consensus forecast of 4.0 percent. Average hourly earnings are up 0.3 percent in February from January and up 4.0 percent year-over-year. On the face of it, the February employment report looks like another in a line of solid reports. However, some of the details point to softer conditions in the labor market.

The monthly average for the payrolls rise is 138,000 for the January-February period, below the quarter average of 289,000 in the fourth quarter 2024 and 157,000 in the third quarter 2024.

Private payrolls are up 140,000 in February. However, this is mainly due to a 73,000 increase in private education and health services. Job gains elsewhere were generally much smaller. There is evidence of cutbacks in areas associated with consumer spending like a16,000 decline in leisure and hospitality, or 6,300 in retail trade. Government jobs are up 11,000, but that is only at the state and local level. Federal government jobs are down 10,000.

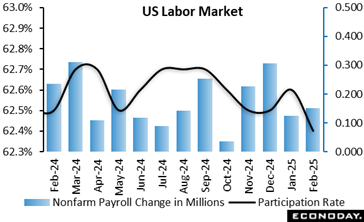

The slight rise in the unemployment rate is not alarming in itself, but it is the result of a 385,000 drop in the labor force to 170.359 million in February with the number of employed down 588,000 to 163.307 and unemployed up 203,000 to 7.052 million. The U-6 unemployment rate – the broadest measure of unemployment – jumps five-tenths to 8.0 percent in February, its highest since 8.2 percent in October 2021. Layoffs and/or stalled hiring is leading to more workers considering themselves as unemployed, among them discouraged workers who are experiencing longer separations from the labor market and/or problems finding new jobs in their field. The labor force participation rate is down two-tenths to 62.4 percent in February.

One indicator of some distress in the labor market is the rise of people working part-time for economic reasons which rose 460,000 to 4.937 million in February. Workers will take part-time employment when they can’t find full-time jobs or take on a second job to improve household finances when prices are up or debt is pressing.

The FOMC will be care not to overreact to a single set of data points, but combined with other evidence, will probably conclude that the labor market and US economy has not yet weakened sufficiently to tip the balance to a need for rate cuts, but it will be more central to the discussions of the risks to the outlook at the upcoming March 18-19 meeting.

GDP

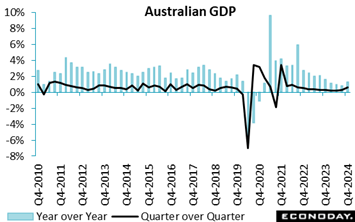

Australia’s GDP expanded 0.6 percent on the quarter in the three months to December, up from the 0.3 growth recorded in the three months to September and just above the consensus forecast of 0.5 percent. The economy has grown at a weak pace for two years, reflecting the impact of tight monetary policy settings. GDP rose 1.3 percent on the year in the three months to December, picking up from 0.8 percent in the three months to September and in line with the consensus forecast.

Household spending and private investment both rose modestly on the quarter, up 0.4 percent and 0.3 percent respectively, while net trade and government spending also made positive contributions to GDP growth. GDP per capita grew 0.1 percent on the quarter after seven consecutive quarters of declines.

Today’s data cover the period in which officials at the Reserve Bank of Australia continued to leave policy rates on hold. At their latest meeting, held last month, officials cut policy rates for the first time since 2020 but indicated that further policy easing remains dependent on the inflation outlook. Today’s data, however, suggest that previous policy tightening is continuing to weigh on demand and activity.

Production

The manufacturing sector experienced a sharp contraction in January 2025, with new orders plummeting by 7.0 percent month-over-month and 2.5 percent year-over-year. This downturn followed a substantially revised 5.9 percent monthly rise and minus 6.5 percent annual fall in December, highlighting the volatility in demand. Large-scale orders were pivotal in these fluctuations, with their exclusion revealing a more moderate 2.7 percent decline.

By sectors, the manufacture of machinery and equipment (minus 10.7 percent) and other transport equipment (minus 17.6 percent) bore the brunt of the slowdown, reversing gains from major orders in December. The computer, electronic, and optical products sector saw a 12.9 percent decline, further dampening overall performance. However, electrical equipment showed resilience, with orders rising by 4.8 percent, offering a glimmer of optimism.

Domestic demand collapsed (minus 13.2 percent), while foreign orders saw a milder 2.3 percent decline, suggesting weaker confidence within the local market. Capital goods orders fell by 11.0 percent, signaling potential caution in long-term investment.

Despite the downturn, turnover increased slightly (0.4 percent), reflecting delayed revenue recognition. The months ahead will determine if this contraction is temporary or a sign of deeper industrial strain.

Business Surveys

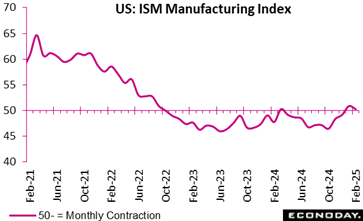

The ISM Manufacturing PMI came in at 50.3 in February, compared to the 50.9 recorded in January, and lower than the 50.5 expected in the Econoday survey of forecasters.

“U.S. manufacturing activity expanded marginally for the second month in a row in February after 26 consecutive months of contraction,” the report says. “Demand weakened, while output stabilized and inputs, for the first time in several months, contributed to PMI growth.”

New orders Index contracted after expanding for three months, production grew at a slower rate compared to January but still expanded for the second month in a row after eight months in contraction.

Prices surged again, and orders’ backlog also rose. On the other hand, employment is down from January’s figure and customers’ inventories also dipped further into “’too low’ territory.”

“Factory output marginally expanded compared to January, indicating that panelists’ companies are being cautious about ramping up output in the face of economic headwinds,” according to the ISM.

“Demand eased, production stabilized, and de-staffing continued as panelists’ companies experience the first operational shock of the new administration’s tariff policy. Prices growth accelerated due to tariffs, causing new order placement backlogs, supplier delivery stoppages and manufacturing inventory impacts,” it added.

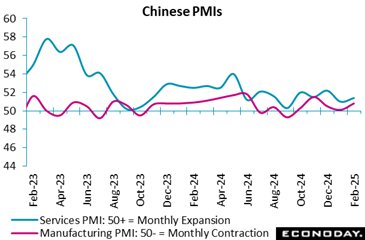

The S&P Global China manufacturing PMI showed subdued but slightly stronger conditions in the sector in February, with the headline index advancing to 50.8 from 50.1 in January. Official PMI survey published over the weekend also showed that conditions in the sector improved in February.

Respondents to the S&P PMI survey reported output and new orders rose at a faster pace in February, while new export orders were reported to have risen for the first time in three months. Payrolls were reported to have been cut for the sixth consecutive month, but the survey’s measure of business confidence improved. The survey also shows input costs rose at a modest pace in February and that firms cut selling prices for the third consecutive month.

The S&P Global PMI composite index for China rose to 51.5 in February, picking up from a four-month low of 51.1 in January and indicating modest growth in the Chinese economy at the start of the year. The business activity index for China’s services sector rose to 51.4 from 51.0, while the headline index for the manufacturing PMI survey, published earlier in the week, also indicated conditions improved modestly in the sector. Official PMI survey data showed subdued conditions in both the manufacturing and the non-manufacturing sector in January.

Respondents to today’s service sector survey reported slightly stronger but still subdued growth in output, new orders, and new export orders in February. The survey showed an increase in payrolls after declines in each of the two previous months and its measure of confidence rose to its highest level since November. Respondents also reported a small fall in input costs, the first decline since mid-2020, and also a small reduction in selling prices.

US Review

Fed’s Powell Still Sees Policy in Good Place, No Rush to Change

By Theresa Sheehan, Econoday Economist

The communications blackout period around the March 18-19 FOMC goes into effect at midnight on Saturday, March 8 and runs through midnight on Thursday, March 20. The last significant remarks from a Fed policymaker were from Chair Jerome Powell on Friday March 7 at the University of Chicago Booth School of Business 2025 U.S. Monetary Policy Forum. Viewed in conjunction with the February Employment Situation, Powell’s comments highlight that the US economy remains in a “good place”. He did not sound the alarm regarding growth against the backdrop of fast-moving developments out of the Trump administration. Powell said, “It is the net effect of these policy changes that will matter for the economy and for the path of monetary policy.”

Powell set the tone going into the next meeting, as one of caution and careful consideration of the incoming data. The FOMC with an uncertain economic outlook, fading job gains, and rising job losses at the same time inflation and inflation expectations are a bit higher. The prescription for the former is to lower rates while the prescription for the latter is to maintain restrictive monetary policy. For the moment, expectation should remain for policy to remain on hold 4.25-4.50 percent for the fed funds target range.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.