The Economy

Monetary policy

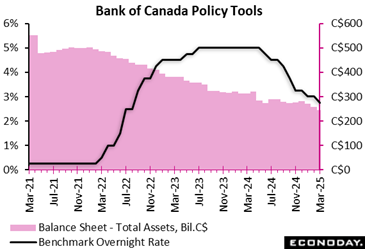

The Bank of Canada, as expected in the Econoday consensus forecast, again cut its target interest rate by 25 basis points from 3.0 percent to 2.75 percent, as the central bank shifts its attention to protecting against the drag on economic activity from punitive tariffs imposed by the United States.

The Bank of Canada, as expected in the Econoday consensus forecast, again cut its target interest rate by 25 basis points from 3.0 percent to 2.75 percent, as the central bank shifts its attention to protecting against the drag on economic activity from punitive tariffs imposed by the United States.

"[H]eightened trade tensions and tariffs imposed by the United States will likely slow the pace of economic activity and increase inflationary pressures in Canada,” the BoC statement said. “The economic outlook continues to be subject to more-than-usual uncertainty because of the rapidly evolving policy landscape.”

The central bank expects growth to slow down in the first quarter of 2025 as the trade conflict negatively affects sentiment and economic activity. The labor market will also be adversely impact, with the BoC noting “warning signs that heightened trade tensions could disrupt the recovery in the jobs market.”

It expects inflation to remain close to its target, rising from 1.9 percent in January to “about” 2.5 percent in March once the suspension of sales taxes expires. In addition, short-term inflation expectations have risen – driven by worries about the impact of tariffs on prices.

“Monetary policy cannot offset the impacts of a trade war,” it said. “What it can and must do is ensure that higher prices do not lead to ongoing inflation.”

“Governing Council will be carefully assessing the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs,” the statement said.

Inflation

China’s headline consumer price index fell 0.2 percent on the year after advancing 0.5 percent in December. The index fell 0.7 percent on the month after increasing 0.7 percent previously, but this decline largely reflects the impact of the timing of lunar new year holidays, which took place mid-February last year, but which started in late January this year. Producer price inflation data also published today showed ongoing weakness in price pressures.

China’s headline consumer price index fell 0.2 percent on the year after advancing 0.5 percent in December. The index fell 0.7 percent on the month after increasing 0.7 percent previously, but this decline largely reflects the impact of the timing of lunar new year holidays, which took place mid-February last year, but which started in late January this year. Producer price inflation data also published today showed ongoing weakness in price pressures.

Excluding the impact of lunar new year holidays, the consumer price index is estimated to have risen 0.1 percent on the year in February, indicating that price pressures at the start of the year remain very subdued. Officials have lowered their target for annual inflation this year to two percent, down from three percent previously, and have also changed the monetary policy stance from "prudent" to "moderately loose". This suggests that policy settings may be adjusted in coming weeks to support economic activity.

China’s headline producer price index fell 2.2 percent on the year in February, little changed from the 2.3 percent decline recorded in January. Headline PPI inflation has been in negative territory since late 2022. The index fell 0.1 percent on the month after a previous decline of 0.1 percent.

Consumer price data also published today showed headline inflation moved into negative territory in February. This largely reflects the impact of the timing of lunar new year holidays, which took place mid-February last year, but which started in late January this year. Excluding this impact, however, consumer price pressures remain subdued.

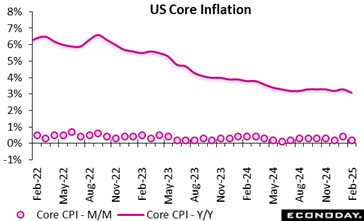

The Consumer Price Index in Feburary rose by just 0.2 percent, following a 0.5 percent jump in January, and a 0.4 percent rise in December. This compares to expectations for a 0.3 percent rise in the Econoday survey of forecasters. The slowdown in the pace of consumer price increases comes after a steep rise in the CPI between November 2024 and January 2025.

The Consumer Price Index in Feburary rose by just 0.2 percent, following a 0.5 percent jump in January, and a 0.4 percent rise in December. This compares to expectations for a 0.3 percent rise in the Econoday survey of forecasters. The slowdown in the pace of consumer price increases comes after a steep rise in the CPI between November 2024 and January 2025.

Over the last 12 months, consumer prices are up 2.8 percent, compared to a 3.0 percent year-over-year rise in January. Expectations were for a 2.9 percent increase.

Core CPI, excluding food and energy prices, rose 0.2 percent, easing off after rising by 0.4 percent in January, and +0.2 percent in December. Consumer prices less food and energy rose 3.1 percent from February 2024, after rising by 3.3 percent on an annual basis in January.

The data might ease concerns, somewhat, that inflation is flaring up again. It remains to be seen, however, the full impact that recently announced punitive tariffs will have on consumer prices. The Federal Reserve will be encouraged by this data, but it alone is unlike to influence the central bank’s decision to hit pause on rate cuts for the foreseeable future.

After rising by 0.4 percent in January, shelter costs rose by 0.3 percent in February (and are up 4.2 percent year-over-year). Food prices increased by 0.2 percent, building on a 0.4 percent rise in January, as grocery prices were flat last month, and restaurant prices rose by 0.4 percent. Energy costs saw a 0.2 percent increase over the month, after jumping by 1.1 percent in January.

Energy prices are down 0.2 percent year-over-year, following a 1 percent rise for the 12 months ending January. Food prices increased 2.6 percent compared to February 2024, compared to a 2.5 percent rise in January.

Employment

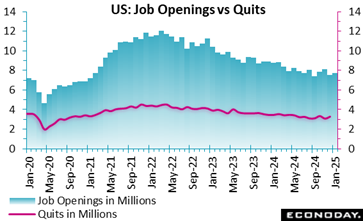

The number of job openings rose to 7.74 million (4.6 percent) in January, from a downwardly revised 7.51 million (4.5 percent) in December and compared to the expectation of 7.5 million in the Econoday survey of forecasters. Job openings are down by 728,000 compared to a year ago.

The number of job openings rose to 7.74 million (4.6 percent) in January, from a downwardly revised 7.51 million (4.5 percent) in December and compared to the expectation of 7.5 million in the Econoday survey of forecasters. Job openings are down by 728,000 compared to a year ago.

January hires were 5.393 million (3.4 percent), after 5.374 million (3.4 percent) in December, and were down by 179,000 compared to January 2024.

The data confirms the softer labor market trend that began in the second half of 2024, but not enough to add to fears of an imminent recession.

The number of total separations was 5.252 million (3.3 percent) in January, vs 5.082 million (3.2 percent) in December. Within separations, quits were at 3.266 million (2.1 percent) after 3.095 million (1.9 percent) in December, while layoffs and discharges came in at 1.635 million (1.0 percent) following 1.669 million (1.1 percent) in December.

Production

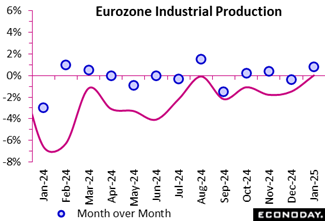

Industrial output rebounded with a 0.8 percent monthly increase after a 0.4 percent decline in December 2024, 0.2 percent points below the consensus, signalling short-term recovery. However, stability in annual production suggests a lack of sustained momentum.

Industrial output rebounded with a 0.8 percent monthly increase after a 0.4 percent decline in December 2024, 0.2 percent points below the consensus, signalling short-term recovery. However, stability in annual production suggests a lack of sustained momentum.

Sectoral trends reveal contrasting dynamics. The 1.6 percent rise in intermediate goods suggests renewed industrial demand, while capital goods grew modestly (0.5 percent), indicating cautious investment. However, the 3.1 percent drop in non-durable consumer goods and 1.2 percent decline in energy production highlight weak consumer demand and potential shifts in energy consumption.

Industrial production stagnated on an annual basis, with notable declines in capital goods (minus 2.7 percent) and intermediate goods (minus 0.8 percent), hinting at reduced long-term investment and supply chain sluggishness. However, the 6.7 percent surge in non-durable consumer goods and 0.9 percent increase in durable consumer goods suggest resilience in consumer-driven industries. Regionally, among the top 4 economies, industrial production fell in Spain (minus 1.0 percent after 2.2 percent), France (minus 1.5 percent after minus 1.0 percent), and Germany (minus 1.8 percent after minus 3.1 percent) on an annual basis.

January 2025 marked a sharp decline in production output, plunging 0.9 percent, its lowest level since May 2020. This downturn follows a brief resurgence in December 2024 (0.5 percent) but extends a longer-term trend of stagnation, with the three-month output also falling by 0.9 percent. The manufacturing sector, the backbone of industrial production, bore the brunt of this decline, contracting by 1.1 percent and dragging down nine of its thirteen subsectors. The sharpest contractions were observed in basic metals and metal products (minus 3.3 percent), other manufacturing and repair (minus 3.3 percent), and basic pharmaceuticals (minus 3.1 percent), highlighting structural weaknesses across key industries.

January 2025 marked a sharp decline in production output, plunging 0.9 percent, its lowest level since May 2020. This downturn follows a brief resurgence in December 2024 (0.5 percent) but extends a longer-term trend of stagnation, with the three-month output also falling by 0.9 percent. The manufacturing sector, the backbone of industrial production, bore the brunt of this decline, contracting by 1.1 percent and dragging down nine of its thirteen subsectors. The sharpest contractions were observed in basic metals and metal products (minus 3.3 percent), other manufacturing and repair (minus 3.3 percent), and basic pharmaceuticals (minus 3.1 percent), highlighting structural weaknesses across key industries.

Meanwhile, the mining and quarrying sector fell 3.3 percent, further compounding the economic strain. In contrast, water supply and sewerage (2.6 percent) and electricity and gas (0.5 percent) offered some resilience, though not enough to counterbalance the downturn. The persistent three-monthly decline, now in its ninth consecutive period, signals deeper industrial malaise. If these contractions persist, broader economic repercussions, including job losses and declining investor confidence, could intensify in the coming months. The latest update leaves the UK RPI at 39 and the RPI-P at 29, meaning that economic activities remain well ahead of expectations in the UK.

US Review

US Data Suggest Ongoing Expansion but Uncertainty Rising

By Theresa Sheehan, Econoday Economist

Heading into the March 18-19 FOMC meeting, the available economic data remain consistent with modest expansion and a healthy labor market, and a resumption of moderation in upward price pressures at the consumer level. In normal times, this would probably mean that the FOMC would consider the risks to the outlook roughly balanced but allow them to set their forecasts with less uncertainty. However, the seismic changes going on in the federal government means that the implications are difficult to parse out. Businesses and consumers are sharing a deeper sense of unease.

The NFIB small business optimism index for February shows that while small businesses expressed greater confidence in November and December in the post-election period, that has rapidly eroded in January and February. The reading of 100.7 in February is down from 105.1 in December, an unusually large decline over a two-month period. The NFIB uncertainty index fell from a record high of 110 in October 2024 to 86 in December, but has now reached 104 in February, the second highest on record.

The University of Michigan consumer sentiment index declined a sharp 9.2 points in February to 64.7. The preliminary reading for March is down a further 6.8 points to 57.9 to its lowest since 56.8 in November 2022. While it is a truism that indexes of consumer confidence do not necessarily reflect actual consumer behavior, falling confidence to these levels should sound an alarm that personal consumption is likely to see a negative effect. The index for consumer expectations – roughly six months from now – is down 9.8 points to a gloomy 54.2 in early March, its lowest since 47.3 in July 2022 and in recession territory.

The University of Michigan survey of consumers points to inflation expectations for one year from now as remaining as elevated as during the worst of the current inflation episode, and the five year outlook – roughly analogous to the FOMC’s “medium term” language – as higher than any time since the early summer of 2008 during the Great Recession and before then in the mid-1990’s. The 1-year measure is at 4.9 percent, up six-tenths from the prior month and the highest since 4.9 percent in November 2022. The 5-year measure is up four-tenths to 3.9 percent, the highest since 4.1 percent in February 1993. The FOMC may be more concerned about inflation expectations losing their anchor.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.