Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

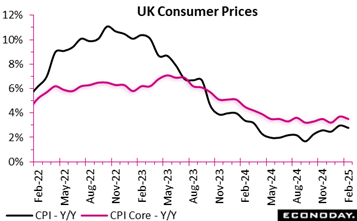

The latest UK inflation report reveals a slight easing in price pressures, with the consumer price index rising by 2.8 percent in February on a year-over-year basis, down from 3.0 percent in January and 0.1 percentage points below the consensus. This easing is primarily driven by core inflation, which excludes volatile items such as energy and food, decreasing to 3.5 percent from 3.7 percent. The service remains stable, with CPI services inflation remaining at 5.0 percent.

Despite the annual decrease, monthly CPI rose by 0.4 percent, a reversal from January’s 0.1 percent fall. This suggests a short-term cost pressure persist. The CPI, including owner-occupiers’ housing costs (CPIH), decreased from 3.9 percent to 3.7 percent on the year, with alcoholic beverages, tobacco and communication costs being the primary inflationary drivers, clothing and footwear, recreation and household services provided some relief.

Core CPIH eased slightly, rising 4.4 percent from 4.6 percent on the year. This reflects slight improvement in underlying inflationary pressures. The divergence between goods and services inflation, with services inflation nearly seven times higher, signals persistent cost-push factors that could challenge monetary policy decisions in the coming months.

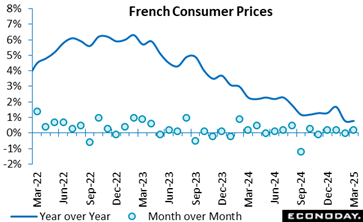

In March 2025, France’s inflation remained subdued, with the consumer price index (CPI) rising by 0.8 percent year-over-year, the same pace as in February, masking diverging trends. On one hand, service prices, especially insurance, and food prices—driven by fresh produce—accelerated. On the other hand, continued declines in energy and manufactured goods prices, alongside a slight slowdown in tobacco inflation, acted as balancing forces.

On a monthly basis, consumer prices rose by 0.2 percent after remaining flat in February. This modest rise was primarily attributed to seasonal increases in clothing and footwear, reflecting typical spring trends. However, price growth in services lost some momentum, and energy prices declined again, further dampening overall inflationary pressure.

The harmonised index of consumer prices (HICP), used for European comparisons, mirrored these patterns, rising 0.9 percent year-over-year and 0.2 percent over the month. Altogether, the data point to a low-inflation environment where household purchasing power remains relatively stable, although sectoral price shifts—particularly in essentials like food and insurance—may still impact consumer sentiment.

GDP

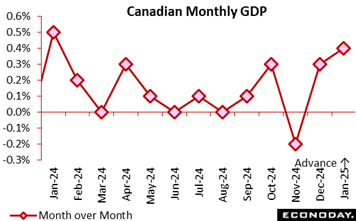

Economic activity in Canada saw a 0.4 percent jump in January, building on December’s revised 0.3 percent rise (previously reported as a 0.2 percent increase). This is above expectations for a 0.3 percent growth rate in the Econoday survey of forecasters, fueled by a flood of goods orders as businesses stockpiled ahead of tariffs imposed by the United States. Compared to January 2024, GDP rose 2.2 percent.

Activity in the goods-producing industries jumped 1.1 percent following a 0.4 percent rise in December, the largest increase since October 2021. All the industrial sectors expanded, with mining, quarrying, oil and gas extraction, as well as manufacturing the main drivers of growth.

Services-producing industries saw just a 0.1 percent rise in activity in January (slowing down from the 0.3 percent increase in December). Retail trade was the major drag on services activity, declining by 0.9 percent following a 2.6 percent growth rate in December.

Demand

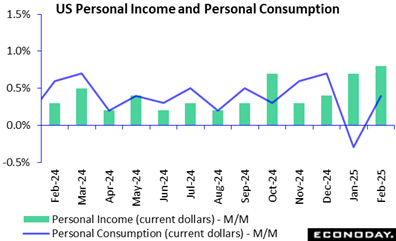

US personal income is up 0.8 percent in February from January, above the consensus of up 0.4 percent in the Econoday survey of forecasters. Wages and salaries are up 0.4 percent in February where the increase is driven by a sharp 1.0 percent rise in manufacturing that probably reflects new labor contracts as well as a demand for skilled workers. Personal income from receipts on assets is up 0.4 percent in February and personal income from current transfer receipts is up 2.2 percent. Government benefits are up 1.8 percent in February and include a 7.1 percent increase in “other” that may be related to downsizing in the federal workforce.

Personal consumption expenditures are up 0.4 percent in February from the prior month, a little below the consensus of up 0.5 percent in the Econoday survey. Spending on durables rebounds to up 1.4 percent in February after declining 4.3 percent in January after demand was exhausted by strong spending late in 2024. Consumers are buying hard goods in advance of expected price increases related to tariffs and possible shortages of some items. Spending on nondurables is up 0.6 percent in February, also picking up after a decline of 0.2 percent in January. Spending on services is up 0.2 percent, suggesting spending on services is trending lower and possibly becoming less of a source of upward price pressures.

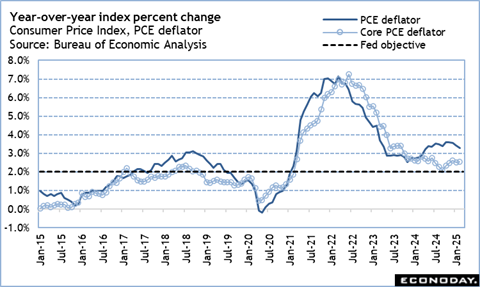

The PCE deflator is up 0.3 percent month-over-month in February, the same as the prior two months. It is steady at up 2.5 percent year-over-year in February. The core PCE deflator is up 0.4 percent in February from January. The month-over-month- percent change has been rising by one-tenth since November. The core PCE deflator is up one-tenth to up 2.8 percent compared to a year ago.

Outside of food and energy, consumer prices as measured by the PCE deflator are trending a bit higher. This will be one factor keeping the FOMC on hold regarding rate cuts as it continues its efforts to get inflation back to the 2 percent target.

Sentiment

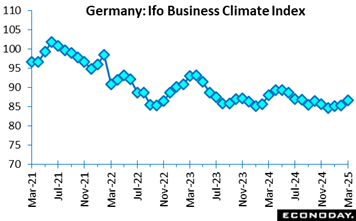

Sentiment in Germany’s business sector shows some improvement, as reflected in the business climate index, up at 86.7 points in March. While companies viewed current conditions slightly more favourably (85.7 vs. 85.0 prior revised), expectations improved more significantly (87.7 vs. 85.6 prior revised), signalling a tentative optimism.

Regarding sectoral trends, manufacturing saw a better outlook with improvement in both current sentiment and future expectations compared to February. Services also improved, with architectural and engineering firms displaying the most significant optimism. Trade showed improvement once again, as both wholesale and retail traders expressed a more positive economic view. Construction also improved, however, a lack of orders still led to strong scepticism in future expectations.

The German economy is showing signs of recovery with all sectors improvement. Despite current challenges, future expectations remain mostly positive. The latest update takes the German RPI to minus 11 and the RPI-P to minus 6. This suggests that the real economy is within market expectations.

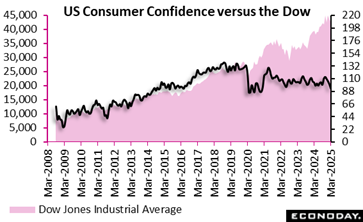

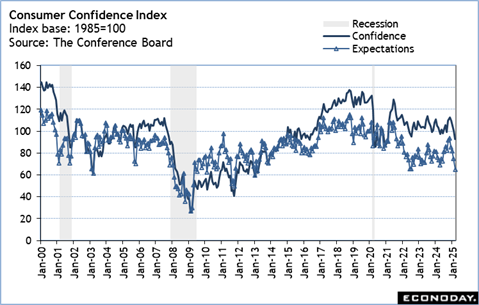

The Conference Board’s US Consumer Confidence Index declined for the fourth straight month in March to 92.9, down from a revised 100.1 (previously 98.3) in February, and below expectations of 94.2 in the Econoday survey of forecasters.

Consumers’ assessment of current business and labor market conditions fell again, while their short-term outlook for income, business, and labor market conditions experienced another sharp decline.

The Expectations Index dropped to the lowest level in 12 years “and well below the threshold of 80 that usually signals a recession ahead.”

There are no bright spots in the report.

“Of the Index’s five components, only consumers’ assessment of present labor market conditions improved, albeit slightly. Views of current business conditions weakened to close to neutral. Consumers’ expectations were especially gloomy, with pessimism about future business conditions deepening and confidence about future employment prospects falling to a 12-year low.”

The Conference Board said the share of consumers expecting a recession over the next 12 months remained steady at a nine-month high, with expectations for future finances falling to the lowest level since July 2022.

“[C]onsumers’ optimism about future income—which had held up quite strongly in the past few months—largely vanished, suggesting worries about the economy and labor market have started to spread into consumers’ assessments of their personal situations,” the report said.

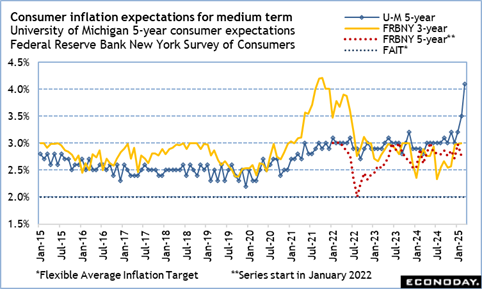

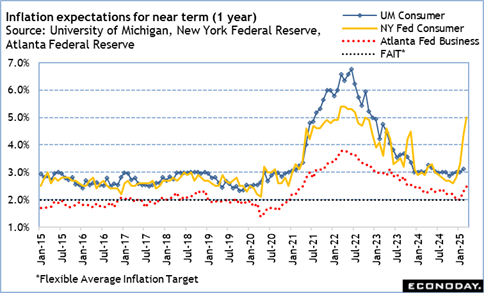

Average one-year inflation expectations jumped to 6.2 percent in March from 5.8 percent in February. “[C]onsumers remained concerned about high prices for key household staples like eggs and the impact of tariffs,” the report said.

On a six-month moving average basis, purchasing plans for both homes and autos declined. However, plans to buy big-ticket items—including appliances and electronics—saw an uptick, “which may reflect plans to buy before impending tariffs lead to price increases,” the Conference Board said.

US Review

Consumer Confidence in Worrisome Decline while Inflation Expectations Jump

By Theresa Sheehan, Econoday Economist

Although Fed Chair Jerome Powell’s observation that survey data does not necessarily reflect the actual behavior of businesses and consumers is accurate, the decline in consumer confidence should be a cause for concern. Consumer confidence measures and their futures indexes are slipping into recessionary territory.

The March Conference Board Consumer Confidence Index is down for a fourth month in a row to 92.9, its lowest since 90.4 in February 2021. Its index for expectations plunged to 65.2 in March, also down for a fourth month in a row and the lowest since 63.7 in March 2013.

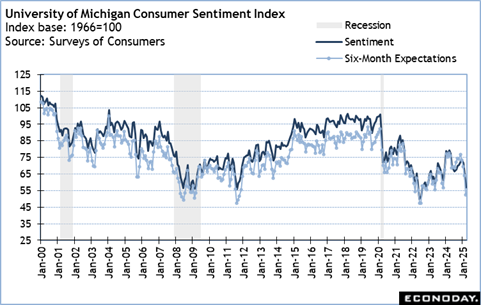

The final March University of Michigan Consumer Sentiment Index is down for the fourth straight month to 57.0, the lowest since56.8 in November 2022. The six-month outlook index is down to 52.6 in March, falling for four months and the lowest since 47.3 in July 2022.

Essentially, whatever improvement in consumers’ attitudes since the end of the pandemic and the period of inflation has been wiped out by uncertainty about the economy, declining hope for improved household incomes in the face of rising costs and worries about job security. Moreover, inflation expectations for businesses and consumers anticipate higher prices in the near term, and more worrisome, higher prices over the medium term. Powell may be correct in that the imposition of tariffs may have a limited duration on upward price pressures, but it also portends that prices will not come down again.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.