Edited by Simisola Fagbola, Econoday Economist

The Economy

Inflation

Year-over-year, Germany’s inflation rate in March is estimated to decelerate to 2.2 percent from 2.3 percent the previous month, indicating a continued easing of price pressures compared to the higher inflation peaks of recent years. On a monthly basis, consumer prices rose by 0.3 percent, suggesting a moderate deceleration from the previous month’s 0.4 percent rise in inflation. The harmonised index, used for EU-wide comparison, shows a similar deceleration from the previous month with a 2.3 percent annual increase and a 0.4 percent monthly rise.

However, core inflation—excluding volatile food and energy prices—is projected at 2.5 percent, slightly above the headline rate. This suggests underlying price pressures remain persistent, likely driven by services, rent, or other non-energy sectors. While inflation is nearing the European Central Bank’s 2 percent target, the stickiness of core inflation could delay policy easing.

In essence, the data shows that headline inflation is gradually aligning with policy targets, but the elevated core figure calls for ongoing monitoring.

Employment

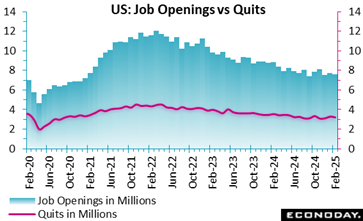

US data on job openings and labor turnover (JOLTS) in February suggests further cooling in the labor market. The number of job openings is down for the third month in a row to 7.568 million at a seasonally adjusted annual rate after a small upward revision to 7.762 million in January. The February level is close to the consensus of 7.600 million in the Econoday survey of forecasters. While the level of job openings is consistent with a healthy labor market, the trend points to sustained deceleration. In February 2024, the level was 8.445 million. The job opening rate is 4.5 in February after 4.7 in January, and down six-tenths from 5.1 in February 2024.

Job openings are down 193,000 for private industries, much of it due to a 126,000 decline in retail and 61,000 in leisure and hospitality. There were some gains in other industries, notably a 134,000 rise in professional and business services, the source of which is unclear. The composition points to concerns about weakness in consumer activity and elimination of open jobs in those areas. Government job openings are down 1,000, mainly in state and local government, with a 6,000 increase at the federal level.

The level of hires has been positive for the past three months, the pace has been declining and is at a meager 25,000 in February to 5.396 million. Private industries added 46,000 to payrolls in February while government hires are down 21,000. Weakness in hiring is widespread in February but got an offset from a sharp rise of 82,000 in professional and business services. It is possible that some businesses are finally able to find skilled workers in a less competitive job market. The hiring rate is unchanged at 3.4 in February from January.

Total separations are down 11,000 to 5.261 million in February, a pause after a large increase of 185,000 in January. Separations in private industry are down 44,000 in February, although broad-based modest declines received some offset from an increase of 47,000 in retail and 27,000 in leisure and hospitality. Separations are up 33,000 in government with federal up 11,000 and state and local up 22,000. The separations rate is unchanged at 3.3 in February from January.

The number of people voluntarily quitting – a subset of separations – is down 61,000 to 3.195 million in February. This is a sharp reversal from an increase of 224,000 in the prior month. The number of people leaving their jobs by choice is trending lower, albeit unevenly. Some may be taking retirement or waiting for a better opportunity if the current period of uncertainty becomes less worrisome in terms of job security. The quits rate remains about unchanged for the past six months and is at 2.0 in February.

However, the level of layoffs and discharges – another subset of separations – is up 116,000 in February to 1.790 million. Layoffs are up 96,000 in private industries and up 21,000 in government. The layoffs and discharges rate is unchanged at 1.1 in February and for most of the past year.

While this data lags the monthly employment report by a month, it complements other labor market data that points to slower hiring and rising job losses, the reverse of the situation that helped the economy recover after the disruptions of the pandemic.

Nonfarm payrolls are up 228,000 in March, well above the consensus of up 131,000 in the Econoday survey of forecasters. However, a net downward revision of 48,000 to nonfarm payrolls in the prior two months takes some of the shine off the March increase. The monthly average increase in nonfarm payrolls is 152,000 for the first quarter 2025 compared to up 289,000 in the fourth quarter 2024.

Private payrolls are up 209,000 in March with payrolls at goods-producers up 12,000 on gains of 13,000 in construction and 1,000 in manufacturing while mining and logging is down 2,000. Service-providers added 197,000 jobs with the largest share from increases of 43,000 in leisure and hospitality, up 48,000 in trade, transportation and utilities, and up 77,000 in private education and health services.

Government payrolls are up 19,000 in March. The rise is entirely due to hiring of 6,000 and 17,000 at the state and local levels, respectively. Federal payrolls are down 4,000.

Average hourly earnings are up 0.3 percent in March from February. The increase from March 2024 is 3.8 percent, the lest since a year-over-year rise of 3.6 percent in July 2024. Pay increases are still outpacing inflation but the size of increases is slipping lower.

The unemployment rate is up a tenth to 4.2 percent in March, the highest since 4.2 percent in November 2024. While the rate remains consistent with a healthy labor market able to absorb new entrants and the unemployed, it has ticked higher the past two months. There is an increase of 77,000 new entrants to the labor force in March. It is not enough to say the labor market is softening appreciably, but it bears watching. The U6 unemployment rate dips a tenth to 7.9 percent in March but remains at a level where it is more difficult for workers on the margins to find jobs.

The labor force is up 232,000 to 170,591 million in March with the number of employed up 201,000 to 163.508 million and unemployed up 31,000 to 7.083 million.

The participation rate is a tenth higher at 62.5 percent in March and remains in a narrow range of 6.24-6.26 percent for the past six months after 62.7 in September 2024.

Overall, Fed policymakers will find more evidence in this report that the labor market remains solid with only minimal signs of softening in March. They will have the April employment report in hand by the time the FOMC next meets on May 6-7. For the moment, the totality of the data for the labor market points to no immediate worry about meeting the maximum employment side of the dual mandate. In turn, this allows the FOMC to focus on the price data and ensuring that inflation gets back to the 2 percent objective consistent with price stability.

Demand

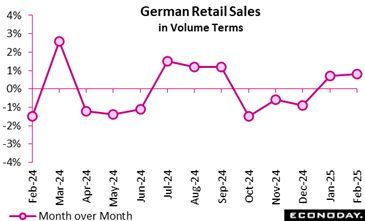

In February, Germany’s retail turnover increased by 0.8 percent compared to January in real terms, continuing the upward trend observed in the revised January data, which showed a 0.7 percent real sales growth. On a year-over-year basis, real retail growth accelerated to 4.9 percent, significantly outpacing January’s revised 3.3 percent growth, indicating strengthening market momentum.

Food retail experienced a moderate monthly rise of 0.8 percent (in real terms), while year-over-year figures indicate a broader inflationary impact, with a 3.3 percent real increase and 5.7 percent nominal increase. The non-food segment posted a 5.2 percent annual real increase, reflecting recovering consumer interest in discretionary spending.

The standout performer was online and mail-order retail, which surged by 15.4 percent in real terms year-over-year—underscoring a substantial shift in consumer behavior towards e-commerce. In the coming months retail sales data could provide clues as to whether consumers are accelerating purchases in anticipation of tariffs.

Overall, the report reflects a robust rebound in retail activity, buoyed by seasonal adjustments and improving consumer confidence. Retailers, particularly in digital channels, appear well-positioned to capitalise on this momentum through 2025.

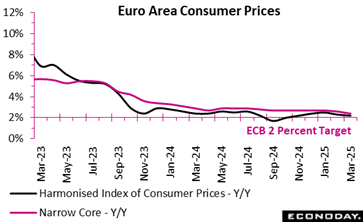

Euro area inflation slightly eases in March 2025, with the annual rate falling to 2.2 percent from 2.3 percent in February, according to the flash estimates. This marginal decline suggests that price pressures are beginning to stabilise, keeping inflation close to the ECB’s 2 percent target.

Among the inflation components, services continue to drive overall price growth, albeit at a slower pace: 3.4 percent in March compared to 3.7 percent in February. This likely reflects persistent wage pressures and robust demand in sectors such as hospitality and transport. Meanwhile, food, alcohol, and tobacco inflation rose to 2.9 percent, indicating that cost challenges in the supply chain are still lingering.

Prices for non-energy industrial goods remained steady at 0.6 percent. Notably, energy prices fell by 0.7 percent following a slight rise in February, reinforcing the deflationary trend in the energy sector. Among the biggest economies in the area, annual inflation fell in Spain (2.2 percent after 2.9 percent) and Germany (2.3 percent after 2.6 percent). However, it increased in Italy (2.1 percent after 1.7 percent) but remained steady in France (0.9 percent after 0.9 percent).

Overall, the euro area’s inflation path appears to be moderating, supported by easing energy costs and stable prices for goods, although inflation in services and food-related sectors suggests that underlying pressures persist. The data may strengthen expectations of cautious monetary policy adjustments in the coming months.

Production

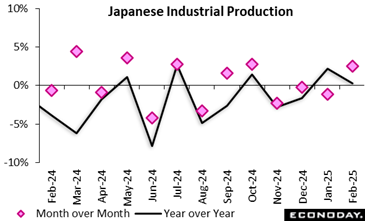

Japan’s industrial production posted a third straight fall on the month in January with a 1.1% slip (vs. consensus -1.4%), dragged down by lower demand for semiconductor-producing equipment and computer chips. The initial reading of a slight 0.3% gain in December has been revised down to a 0.2% dip that follows a 2.2% slump in November and a 2.8% jump in October.

The Ministry of Economy, Trade and Industry said nine out of the 15 industries recorded gains while six showed declines. METI’s survey of producers indicated that output would rebound a solid 2.3% in February, led by output of semiconductor-producing equipment and computer chips, before slipping back 2.0% in March, when vehicle and general machinery productions is seen falling.

From a year earlier, factory output bounced back 2.6% in payback for the 6.7% plunged in January 2024 that was triggered by suspension of all domestic production by Toyota Motor group firm Daihatsu over a vehicle safety scandal from late December until mid-February, which had a widespread impact beyond the auto industry. Toyota also suspended shipments of 10 models after its supplier Toyota Industries admitted to cheating on engine testing. The rebound followed decreases of a revised 1.6% in December and 2.7% in November and a 1.4% gain in October. It was largely in line with the consensus forecast of a 2.4% rebound.

The ministry maintained its assessment, saying industrial output is "taking one step forward and one step back." It said it will keep a close watch on how global economic growth evolves.

Business Surveys

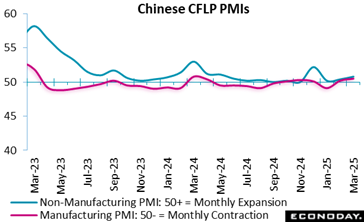

Official Chinese PMI survey data show improved conditions in China’s aggregate economy in March. The headline index for the CFLP manufacturing rose from 50.2 in February to 50.5 in March, indicating modest expansion in the sector for the second consecutive month, while the non-manufacturing PMI also rose from 50.4 to 50.8. The composite index covering the entire economy rose from 51.1 in February to 51.4 in March.

The headline index for the manufacturing and non-manufacturing PMIs were just above the consensus forecasts of 50.3 and 50.6 respectively.

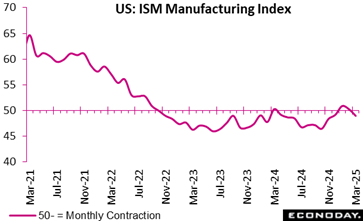

The ISM manufacturing index showed slightly faster than expected contraction in March from February with a range of worrisome declines in business activity and upward price pressures largely related to tariff effects.

The ISM’s index dipped to 49.0 from 50.3 in February, below the 49.5 figure anticipated in the Econoday consensus. New orders fell to 45.2 from 48.6 and production was down to 48.3 from 50.7, declines which reflected "demand confusion" flowing from tariffs, ISM said. Employment was notably weaker at 44.7 from 47.6 with job cuts mostly implemented by attrition and freezing open positions.

The prices index rose again to 69.4 from 62.4, showing accelerating price pressures. ISM said purchasers were looking to buy supplies domestically in response to tariffs and that was putting upward pressure on input costs.

US Review

Powell in No Rush to React to Tariff Scare

By Theresa Sheehan, Econoday Economist

At the end of the week, Fed Chair Jerome Powell offered a carefully balanced assessment of the US economy and the outlook for monetary policy. He described the economy as being in a “good place” despite the high levels of uncertainty as the Trump administration goes about closing programs and agencies and setting new tariff policy. Powell maintained that the FOMC is well-positioned to set monetary policy against the risks of higher unemployment and/or higher inflation. He said the FOMC can afford to “step back” and get some “clarity” as the data reports come in in the weeks before the May 6-7 FOMC meeting.

In the meantime, the March data on payrolls and unemployment presented a picture of a healthy labor market with moderate hiring, modestly rising earnings, low unemployment, and a stable participation rate. The March employment report along with the other reports related to the labor market show no immediate problems in fulfilling the maximum employment side of the Fed’s dual mandate. Powell acknowledged that the tariffs announced on April 2 were “higher than expected” but are now a known quantity whose actual impact will be revealed, and eventually incorporated into FOMC policy decisions.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.