Edited by Simisola Fagbola, Econoday Economist

The Economy

Chinese Inflation

China’s headline consumer price index fell 0.1 percent on the year in March after dropping 0.7 percent in February and fell 0.4 percent on the month after a previous decline of 0.2 percent. Food prices fell 1.4 percent on the year, partly offset by an increase of 0.2 percent in non-food prices. Producer price inflation data also published today showed ongoing weakness in price pressures.

Officials have lowered their target for annual inflation this year to two percent, down from three percent previously, and have also changed the monetary policy stance from “prudent” to “moderately loose”. Global trade tensions and market volatility, however, have increased risks to the economic outlook for China and further complicated the policy decisions for officials.

Today’s data were slightly weaker than the consensus forecast for a year-over-year increase of 0.1 percent in the CPI.

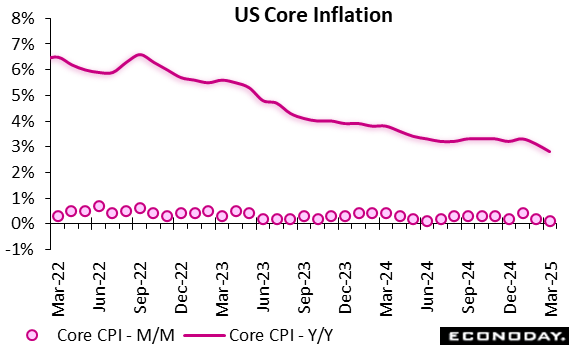

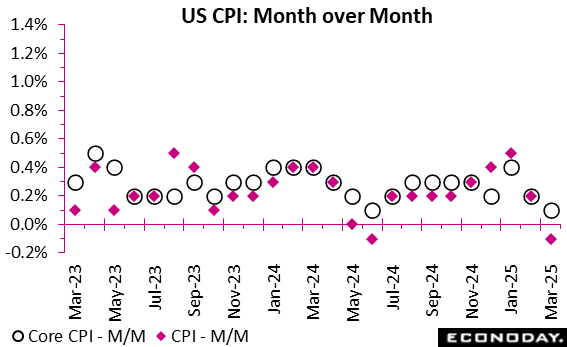

The Consumer Price Index in March declined by 0.1 percent, following a 0.2 percent uptick in February, and a 0.5 percent jump in January. This compares to expectations for a 0.1 percent rise in the Econoday survey of forecasters. The slowdown in the pace of consumer price continues after a steep rise in the CPI between November 2024 and January 2025.

Over the last 12 months, consumer prices are up 2.4 percent, compared to a 2.8 percent year-over-year rise in February. Expectations were for a 2.6 percent increase.

Core CPI, excluding food and energy prices, are up by just 0.1 percent, easing off further after rising by 0.2 percent in February, and +0.4 percent in January. Consumer prices less food and energy rose 2.8 percent from March 2024, after rising by 3.1 percent on an annual basis in February.

The data might ease concerns, somewhat, that inflation is flaring up again. However, this could be the calm before tariff-driven storm hits – with many predicting the inflationary impact on consumer prices will happen by mid-2025. The Federal Reserve will be encouraged by this data, but it is unlikely to influence the central bank’s decision to hit pause on rate cuts for the foreseeable future.

After rising by 0.3 percent in February, shelter costs rose by 0.2 percent in March (and are up 4 percent year-over-year). Food prices jumped 0.4 percent, picking up the pace again after slowing down to a 0.2 percent rise in February, as grocery prices were flat last month, and restaurant prices rose by 0.4 percent.

Exiting the winter-fueled spike in utility bills, energy costs fell by 2.4 percent over the month (dragged down by a 6.3 percent plunge in gasoline prices), after a 0.2 percent increase in February.

Energy prices are down 3.3 percent year-over-year, following a 0.2 percent dip for the 12 months ending February. Food prices increased 3 percent compared to March 2024, compared to a 2.6 percent rise in February.

Demand

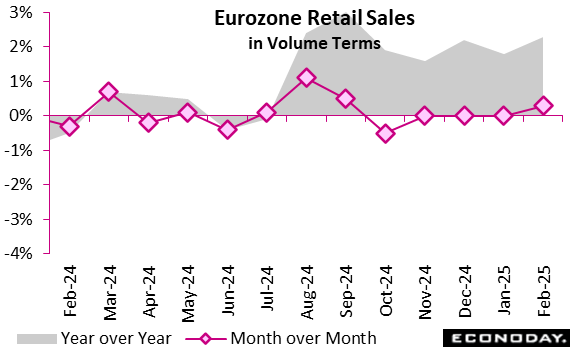

Retail trade in the euro area increased by 0.3 percent in February compared to January, following a flat start to the year due to the revisions for January. This suggests a cautious rebound in consumer activity amid broader economic uncertainty. On an annual basis, retail sales grew by a more notable 2.3 percent, reflecting a recovery in household demand across key sectors.

All major retail categories contributed to the month-over-month increase in February. Sales of food, drinks, and tobacco, as well as non-food items (excluding automotive fuel), grew by 0.3 percent, indicating a balanced spending pattern. Automotive fuel sales also increased by 0.2 percent, suggesting a slight rise in mobility or transportation activity.

Compared with February 2024, the annual gains were more pronounced. Non-food retail led the way with a 2.5 percent rise, while food and beverages grew by 1.9 percent, and automotive fuel sales rose 0.7 percent. These figures suggest a gradual return of consumer confidence, with spending strengthening across both essential and discretionary goods.

Indeed, the euro area’s retail sector is gaining ground, driven by broad-based improvements, although the pace remains cautious amid evolving economic conditions.

Production

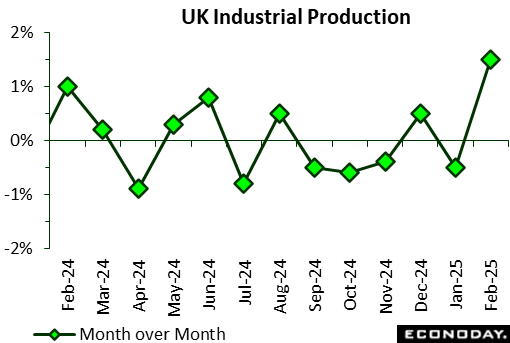

February 2025 marked a strong rebound in UK production output, rising by 1.5 percent after a subdued January, signalling renewed industrial energy. The surge was driven chiefly by manufacturing, which leapt 2.2 percent, supported by gains in electricity and gas (2.0 percent) and water supply and sewerage (1.1 percent). Only mining and quarrying weighed negatively, falling 3.0 percent.

The manufacturing sector’s recovery was broad, with output rising in 10 out of 13 subsectors—six of which had declined in January—pointing to a turnaround in business confidence and operational capacity. Notably, computer, electronic and optical products posted an impressive 9.8 percent increase, possibly reflecting rising global tech demand. Pharmaceuticals (4.4 percent) and transport equipment (1.8 percent) also contributed strongly, suggesting resilience in high-value production sectors.

Over the three months to February, production grew 0.7 percent, reflecting sustained recovery. Manufacturing led this trend (0.6 percent), aided by modest gains in utilities, although the ongoing dip in mining (minus 0.7 percent) tempered overall progress.

These figures suggest that UK production is regaining strength, with technology and pharmaceuticals offering promising signs of industrial dynamism amid an otherwise mixed economic backdrop.

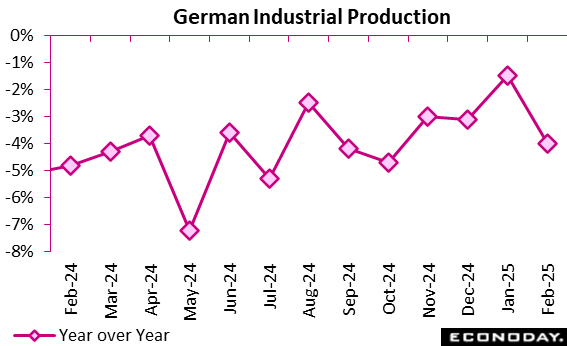

In February, Germany’s industrial output contracted by 1.3 percent from the previous month and fell 4.0 percent year-over-year, highlighting persistent weaknesses in key sectors. While the broader three-month trend showed a slight 0.1 percent increase, this did not mask sector-specific downturns. The construction industry led the decline with a 3.2 percent drop, followed by steep falls in food production (minus 5.3 percent) and energy output (minus 3.3 percent), reflecting a combination of seasonal factors and structural pressures.

Despite this, there were glimmers of resilience—particularly a 3.3 percent rise in electrical equipment manufacturing and a 0.2 percent increase in capital goods production, suggesting ongoing investment in high-tech and industrial infrastructure. However, these gains were offset by declines in consumer goods (minus 3.0 percent) and intermediate goods (minus 0.4 percent), indicating fragile domestic demand.

Energy-intensive industries remain under pressure, falling 0.6 percent month-over-month and 4.0 percent year-over-year, as high energy costs and global uncertainty continue to constrain production. While January’s gains (2.0 percent) provided a brief uplift, February’s performance signals a cautious outlook for industrial recovery in early 2025.

Sentiment

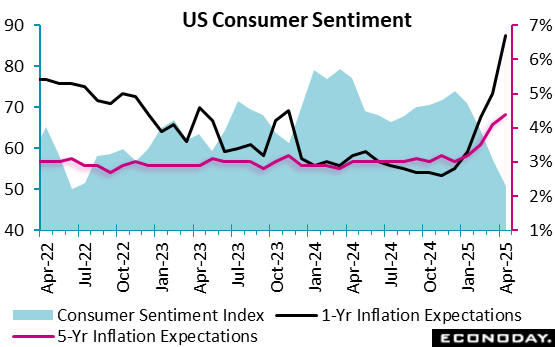

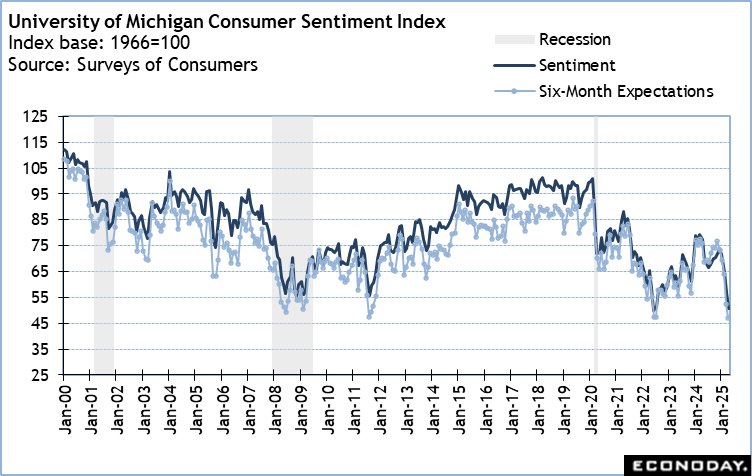

U.S. consumer sentiment continues its downward spiral – declining each month so far in 2025 – with April’s preliminary estimate coming in at 50.8 vs. March’s final reading of 57.0 and 64.7 in February, below expectations for 55.0 in the Econoday survey of forecasters.

“Consumers report multiple warning signs that raise the risk of recession: expectations for business conditions, personal finances, incomes, inflation, and labor markets all continued to deteriorate this month,” the report says. “The share of consumers expecting unemployment to rise in the year ahead increased for the fifth consecutive month and is now more than double the November 2024 reading and the highest since 2009.”

The report notes that the survey collected responses before the announcement of the 90-day pause in higher reciprocal tariffs.

This decline in sentiment was “pervasive and unanimous” across age, income, education, geographic region, and political affiliation. It has plummeted more than 30% since December 2024.

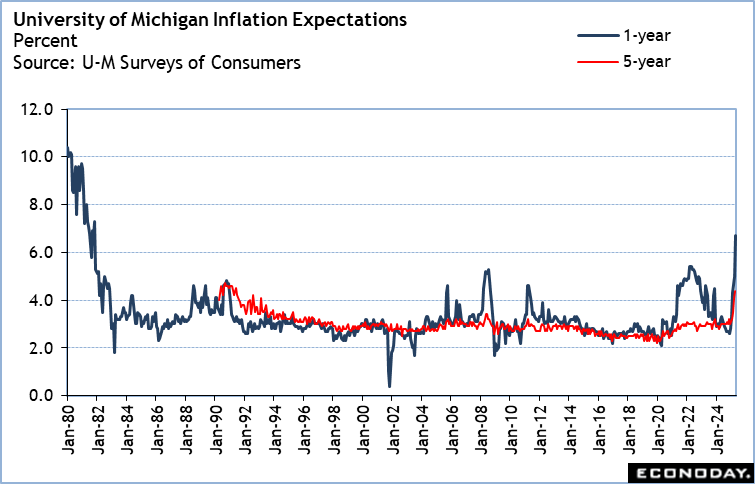

The preliminary year-ahead inflation expectations surged to 6.7 percent in April, jumping from 5 percent in March. This is the highest reading since 1981 and marks four consecutive months of unusually large increases.

Long-run inflation expectations in April went up to 4.4 percent from 4.1 percent last month.

US Review

Sentiment Surveys Show Deepening Gloom on Economy, Rising Inflation Expectations

By Theresa Sheehan, Econoday Economist

At the end of the April 11 week, data related to the near-term outlook shows that business and consumers are deeply concerned about the future of the economy.

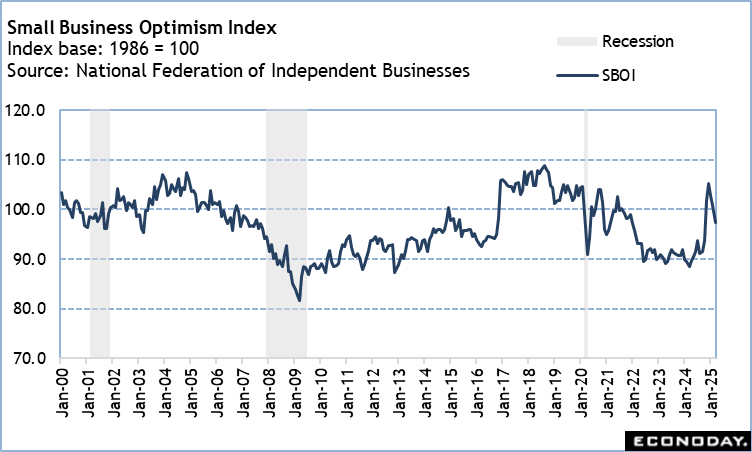

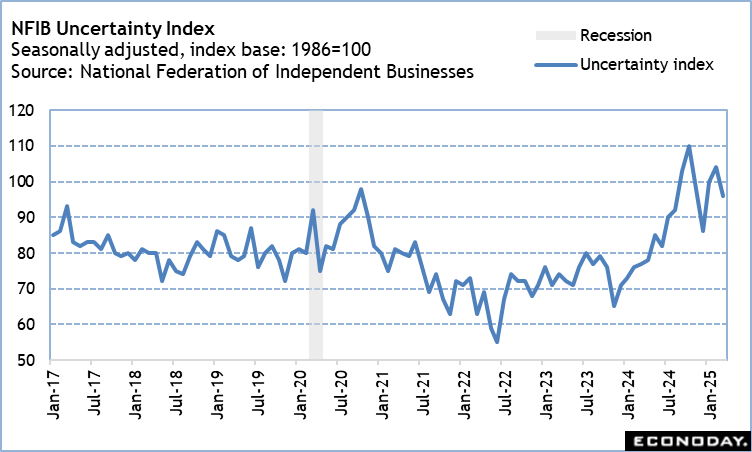

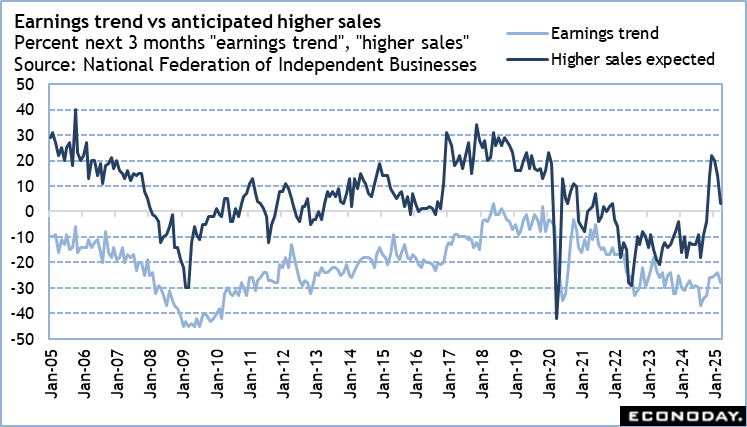

The March NFIB small business optimism index of 97.4 was below the 51-year average of 98 for the first time since 93.7 in October 2024. The post-election bounce has nearly worn off. Seven of 10 components are down for March, two are up, and one is unchanged. Importantly, there is a precipitous slide in two forward-look components – expectations for the economy to improve and higher sales expectations. If the NFIB uncertainty index shows a 4-point improvement to 96 in March, it remains unusually elevated.

The University of Michigan consumer sentiment index fell 6.2 points to 50.8 in the preliminary April report, barely above the record low of 50.0 in June 2022. The current conditions index fell 7.3 points to 56.5, the lowest since 46.6 in October 2022. The expectations index – for conditions about 6 months from now – dipped 5.4 points to 47.2, the lowest since 47.3 in July 2022. The expectations index is well into recessionary territory for the near future.

There is bad news for the FOMC in the readings of inflation expectations. The 1-year inflation expectations measure ballooned to 6.7 percent in early April from 5.0 in March, and which hasn’t been seen since 1981 when the Volcker Fed was working to break the back of inflation. Of course, for monetary policy, it is the medium term which is more important. However, 5-year inflation expectations measure is up to 4.4 percent in early April from 4.1 percent in March. This sort of reading has not been seen since 1991. While a lot of this can be attributed to the whiplash of news related to tariffs, Fed policymakers will have a hard time reassuring the public that inflation is not and will not be as bad as the surveys suggest, and that inflation expectations have not lost their anchor and along with it the Fed’s credibility as an inflation fighter. The FOMC will not be cutting rates unless and until it is clear the swing higher is of temporary duration and will calm down once White House policy looks stable.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.