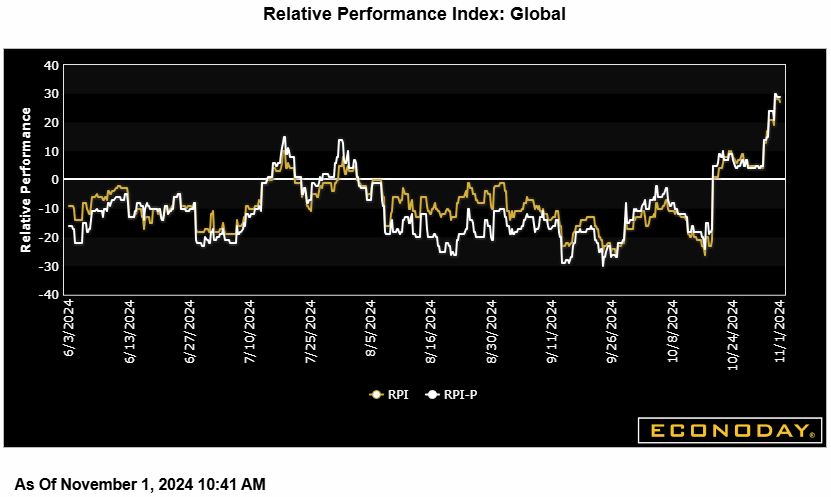

Politics may dominate activity in financial markets this week but the data remain key to monetary policy and five major central banks will be making policy announcements. At 23, Econoday’s Relative Economic Performance Index (RPI) shows recent global economic activity moving ahead of forecasts but only after almost three months of sustained underperformance. As such, with inflation trends in general still headed south, many central banks remain poised to ease further.

In the U.S., following a messy, but probably soft October employment update, and just ahead of Tuesday’s presidential election and Thursday’s FOMC announcement, the RPI stands at minus 1 and the RPI-P at 4. Accordingly, the latest data show overall economic activity running pretty much as expected and leave a high likelihood of a 25 basis point cut by the Federal Reserve this week.

In Canada, zero economic growth in August was in line with forecasts but the RPI (minus 20) and RPI-P (minus 13) both still slipped further below zero. On current trends, another cut in Bank of Canada interest rates in December remains firmly on the cards.

In the Eurozone, the RPI (22) and RPI-P (12) crept further into positive surprise territory, in part reflecting a slightly firmer than forecast flash October inflation report. An ECB interest rate cut next month still seems very probable but a full 50 basis point move now looks rather less likely.

In the UK, mainly second tier data saw the RPI slip to minus 34 and the RPI-P to minus 16. Overall economic activity is falling somewhat short of expectations and mainly due to surprisingly weak prices – the ideal combination for a cut in Bank Rate this week.

In Switzerland, Friday’s deluge of surprisingly weak data saw the RPI slide to minus 28 and the RPI-P drop to minus 20. With core inflation increasingly in danger of falling below zero, the Swiss National Bank would seem to have little choice but to ease policy yet again in December.

In Japan, a very mixed suite of data saw the RPI and RPI-P close out the week at 6 and minus 7 respectively, essentially showing economic activity in general matching market expectations. The unchanged decision from the central bank was widely expected but on current trends another hike in interest rates in December is at least a possibility, especially should upcoming inflation reports surprise on the upside.

Meantime, fresh signs of life in the Chinese economy lifted both the RPI and RPI-P to 64, their highest readings since the end of March and offering early, but only very tentative, signs that the latest stimulus packages might work.

Econoday’s RPI provides a handy summary measure of how an economy has recently been evolving relative to market expectations.

A reading above zero means that the economy in general has been performing more strongly than expected and vice versa for a reading below zero. The closer is the value to the maximum (+100) or minimum (-100) levels, the greater is the degree to which markets have been under- or over-estimating economic activity. A zero outturn would imply that, on average, the market consensus has been correct. Note too that the index is sensitized to place extra weight upon those indicators that investors consider to be the most important.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.