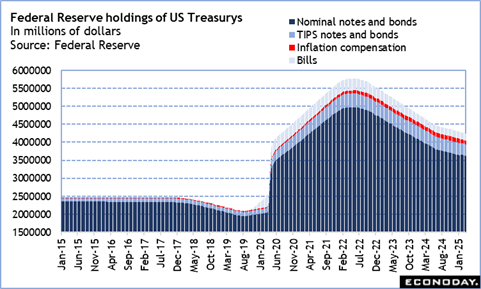

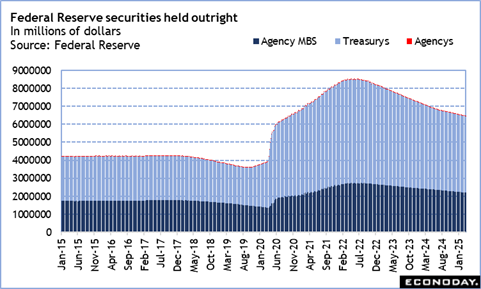

In May 2022, the FOMC announced a program to reduce the size of its holdings of US treasuries and agency mortgage-backed securities which had ballooned to just over $8.5 trillion in May 2022 at the end of its fourth large scale asset purchases undertaken to support the US economy from the shocks of the global pandemic and disruptions to the US economy.

The prior three large scale asset purchase programs (so-called quantitative easing or QE) had previously brought the size of the Fed’s holdings at reserve banks up to just above $4.2 trillion in September 2017. Thereafter the FOMC began a program to reduce the size of the balance sheet. By October 2019 at the end of the program, the balance sheet was reduced by about $665 billion to around $3.6 billion.

The fourth large scale asset purchase program began in March 2020, first to provide liquidity, then to support the economy’s recovery through stimulus. The program ended in January 2022.

The program to begin reducing the current holdings was announced in May 2022 and began in June 2022. The program began with reinvestment caps of $30.0 billion for US treasuries and $17.5 billion for agency mortgage-backed securities in June, July, and August. It was increased as announced to $60.0 billion in US treasuries and $35.0 billion in agency mortgage-backed securities in September.

The caps remained the same until the FOMC announced in May 2024 that beginning in June, the cap on US treasuries reinvestments would be reduced to $25.0 billion while the cap on mortgage-backed securities would remain at $35.0 billion. It was noted that the cap on mortgage-backed had yet to be reached in any given month and that leaving the cap unchanged was consistent with gradually returning the Fed’s holdings to an all-US treasuries composition. Two-thirds of the current balance sheet composition is US treasuries.

Fed Chair Jerome Powell said the decision meant that while it would take longer to bring down the size of the Fed’s balance sheet, it would enable reductions to go further and without disruptions to markets.

Powell offered much the same reasoning after the March 18-19 FOMC when the committee decided to further slow the pace of reduction by bringing the cap on reinvestments in US treasuries down to $5.0 billion while leaving the cap on reinvestments in mortgage-backed securities at $35.0 billion. The new cap will take effect in April.

In his March 19 press conference, Powell emphasized that this is a technical decision and unrelated to monetary policy. He added that the FOMC made no determination on the ultimate size of the Fed’s holdings of US treasuries and did not project how quickly the mortgage-backed securities holdings would diminish.

Many of those securities are backed by mortgages taken out while rates were historically low. Borrowers with exceptionally low rates are less likely to sell their home to up- or down-grade while rates are twice what they were at the time when the mortgage issued depending on the implications for monthly housing costs. Few of these mortgages will be refinanced unless the holders have compelling reasons to take out some equity.

In any case, since the beginning of the current program in June 2022, the total holdings of US treasuries and agency mortgage-backed securities are down about $2.0 trillion from the peak of $8.5 trillion in May 2022. Powell said that the current holdings still constitute “abundant” reserves rather than the “ample” reserves level the FOMC would like to reach. He did say that the first hints that reserves are a little tighter are appearing. The FOMC’s go slower and get further approach means that it will be a longer time before that goal is reached.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.