Expectations are that the FOMC will leave rates unchanged after their deliberations on September 19-20. These are unlikely to be disappointed.

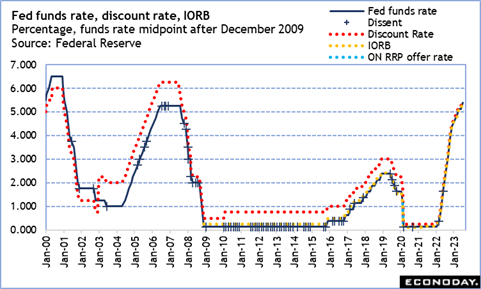

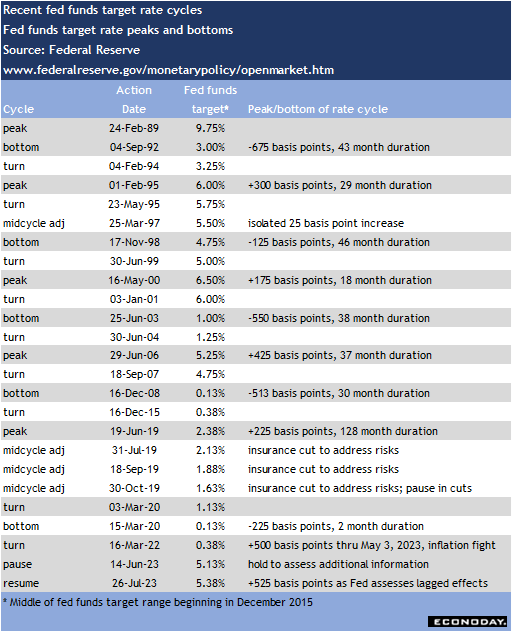

The FOMC is unanimous in its determination to quell inflation and bring it back to the 2 percent flexible average inflation target. Where any disagreement is likely to emerge is in the size and/or timing of more increases in short-term rates, and if indeed any more increases are needed. The previous quarterly summary of economic projections suggested that restrictive monetary policy would reach its current peak by the end of 2023. With 525 basis points of rate hikes in place since the March 2022 meeting, at this next meeting, the FOMC will have more data to evaluate the proverbial “long and variable lags” in the transmission of interest rate policy and to consider their next steps.

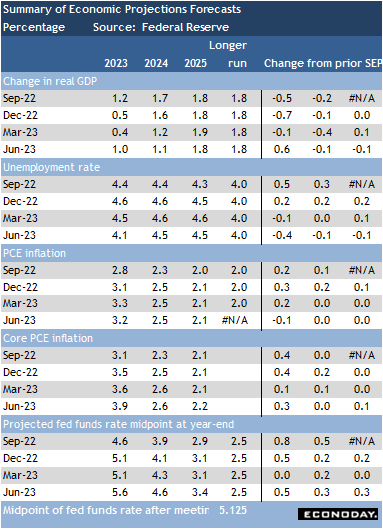

The current crop of economic data suggests that monetary policy is hitting a sweet spot. The labor market is cooling, but healthy, and seeing supply and demand come back into balance. Moderate economic expansion continues despite forecasts for a period of below trend growth. Anchored inflation expectations provide evidence that the Fed’s efforts to fight inflation are credible even if, when the fight is finished, inflation is expected to remain above pre-pandemic levels. Finally, inflation measures indicate the pace of wage and price increases are slowing noticeably although the data are a bit bumpy.

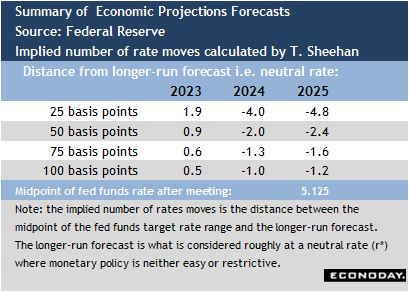

When the FOMC updates its quarterly forecasts at the September meeting, the discussion will focus on progress and whether enough has been made to support a pause in the current tightening cycle. If the FOMC determines that no more hikes are needed in the near future, then the next question will be how long will the pause last, how long will restrictive policy need to stay in place for the 2 percent target to be reached?

With many risks and uncertainties still out there, the FOMC will probably continue to avoid giving forward guidance on policy and remain on a meeting-by-meeting basis. Some policymakers – among them Chair Jerome Powell – have observed that getting inflation back to target and calibrating monetary policy is reaching a stage where gains are harder to achieve and setting rates becomes a matter of caution that can be undertaken with less urgency.