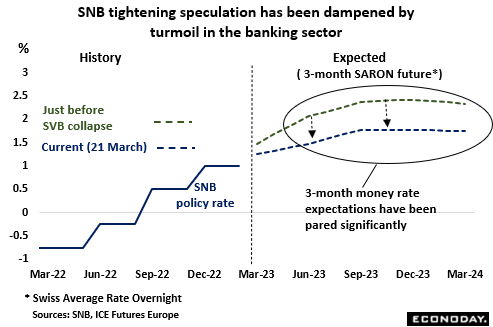

In line with most other major central banks, the SNB had been expected to extend its tightening cycle this week. Having last raised its policy rate by 50 basis points to 1.0 percent in December, another 50 basis point increase was widely anticipated at Thursday’s Monetary Policy Assessment (MPA). However, the turmoil in global banking markets initially triggered by the collapse of Silicon Valley Bank (SVB) in the U.S. and subsequent enforced purchase of Credit Suisse by Switzerland’s largest bank, UBS, has clouded the outlook for monetary policy both at home and abroad. The interest rate decision will at least in part be determined by how markets perform between now and the central bank’s announcement. Should the move on Credit Suisse and additional liquidity boosting measures announced by other central banks restore confidence, another hike in the policy rate is very likely. Otherwise, the SNB may well want to be more cautious in its actions having already provided CHF100 billion to UBS and Credit Suisse as part of last Sundays’ rescue package. For now, the market consensus looks to be a 25 basis point increase in the policy rate to 1.25 percent, boosting the cumulative tightening to date to 200 basis points, but that could easily change by Thursday.

Shortly before the news of the collapse of SVB and run on Credit Suisse stocks, hawkish comments from the central bank and some firm Swiss inflation data had left financial markets expecting significant tightening by the bank throughout 2023 with 3-month money rates peaking just below 2.5 percent in December. However, the high has now been slashed to around 1.75 percent and rates are currently expected to be back down at almost 1.0 percent by the end of next year.

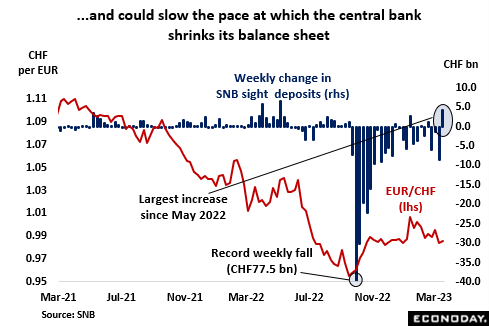

Meantime, prior to the onset of the banking troubles, the SNB had been steadily shrinking its balance sheet, mainly through disposals of international assets, with a view to negating the potentially inflationary impact of excess liquidity sloshing around the money markets. From a peak level of around CHF1.07 trillion in May 2022, total assets had been pared back to CHF884.6 billion by January. Importantly, the foreign currency sales have had little impact on the franc which, while remaining largely on the strong side of parity, since last September has actually lost a little ground versus the euro. In December, the central bank reiterated its view that it was prepared to intervene on both sides of the FX market as necessary in order to keep the exchange rate broadly stable and it can be expected to issue a similar statement on Thursday. Indeed, in seeking to do just that, the bank may be forced to raise domestic rates just to counter any positive effects on the euro of ECB tightening. In any event, the central bank is clearly determined to make further sales but for now, efforts to stabilise the banking sector might dictate otherwise. To this end, of note in the week to 17 March, sight deposits at the bank rose by more than CHF4 billion, their steepest increase since May last year. From a political perspective, a smaller balance sheet has also become all the more pressing with sharp swings in financial markets in 2022 resulting in the bank posting a record CHF132.5 billion loss and rendering it unable to provide the cantons and government with their usual dividend, worth some CHF6 billion in 2021.

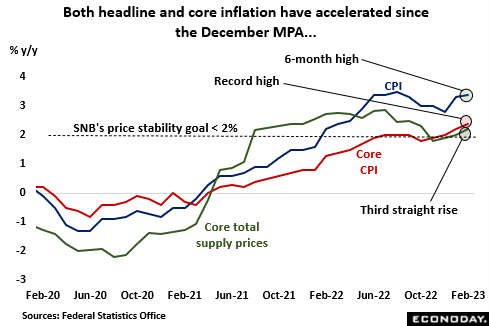

Importantly, inflation has accelerated in recent months. February’s yearly rate showed a third straight increase and, at 3.4 percent, was just a tick below this century’s record high posted last August. More significantly, the core rate went one better, climbing for a fourth straight month to 2.4 percent and setting a new peak. Significantly too, the mid-quarter report indicated a broad-based pick-up in the pace of price rises, warning that high inflation is becoming increasingly entrenched. Moreover, the increase in the overall rate would have been steeper but for a deceleration in import prices where the inflation rate has fallen from a peak of 8.6 percent last August to currently 4.9 percent. Over the same period, the domestic rate has climbed from 1.8 percent to 2.9 percent. This will not sit at all well with the SNB. To make matters worse, underlying pipeline pressures have also become more intense since November with annual core total supply price inflation climbing from 1.8 percent to 2.2 percent in February, a 4-month high.

The labour market is showing some early signs of loosening but remains very tight. The jobless rate has stabilised but at its lowest level in more than two decades and, despite edging higher in 2023, the number of people unemployed per job vacancy is only a fraction above its all-time trough. Vacancies have been trending down since the middle of last year but only very recently have they fallen at a pace that should signal a clear cooling in demand. Even then, just last month the president of the Swiss Employers’ Association stressed that a shortage of workers was the main obstacle to the Swiss economic expansion and wants to see an increase in the potential workforce by some 300,000 people.

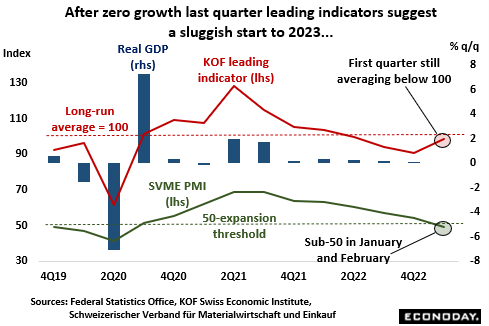

Real GDP growth dried up at the end of 2022. However, a respectable overall performance by domestic demand – within which household spending, government consumption and, in particular, gross fixed capital formation all made positive contributions – was masked by a significant deterioration in the foreign trade balance. Even so, the signs are that higher borrowing costs are impacting economic activity. The construction sector has been struggling for some time now and prices of single-family homes fell last quarter for the first time since before the pandemic, a development that will not displease the SNB. Consumer confidence improved in January for the first time since the middle of 2021 but was still a long way short of its historic norm and buying intentions were notably weak. In addition, February’s SVME PMI was again below the 50-expansion threshold while last month the KoF’s leading indicator only just reclaimed its long-run average having fallen short every month since May 2022. The bottom line is that although recession does not look a real threat, the economy is likely to remain quite sluggish. The State Secretariat for Economic Affairs (SECO) last week forecast 2023 growth at 1.1 percent.

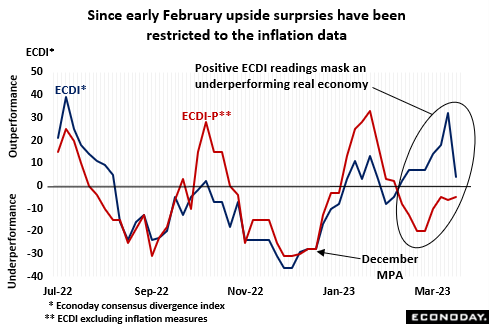

In fact, economic news since the December MPA has been mixed with roughly equal upside and downside surprises. However, since the start of February, positive readings on the ECDI, which measures overall economic activity versus expectations, have masked generally disappointing developments in the real economy. Hence, the ECDI-P has been consistently below zero. This means that where the data have been stronger than forecast, the shocks have been concentrated in the inflation reports, a point that will not be wasted on the SNB.

In sum, domestic and overseas banking issues have made what looked likely to be a straight forward March MPA a good deal more complicated. On current trends, monetary policy is probably not tight enough for the SNB to achieve its price stability goals so the central bank will be keen to raise interest rates again. As such, should confidence in the banking sector be restored quickly, even another 50 basis point increase on Thursday might still be a possibility. Otherwise, a 25 basis point move could be seen as a useful short-term compromise but, should markets deteriorate much further, expect no change until conditions become a good deal more stable. All that said, bear in mind that the SNB has wrong-footed financial markets in the past and, if necessary, will no doubt be prepared to do so again this week.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.