With the first FOMC meeting of 2025 on the near horizon — January 28-29 – Fed policymakers are going to be carefully parsing the available data on inflation and inflation expectations.

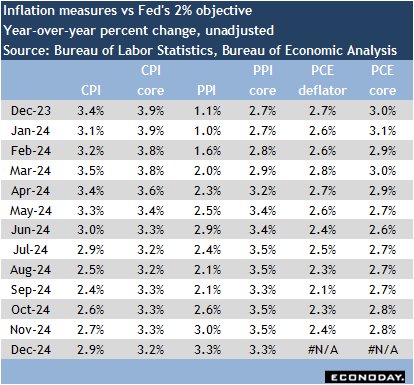

The FOMC will only have the CPI and PPI for December in hand since the PCE deflator for December won’t be reported until Friday, January 31 at 8:30 ET.

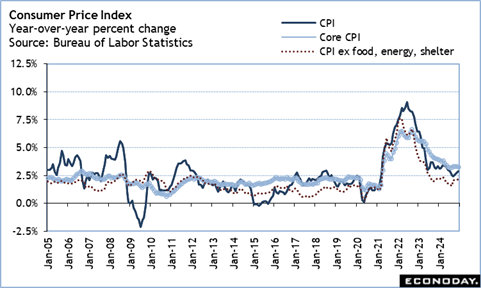

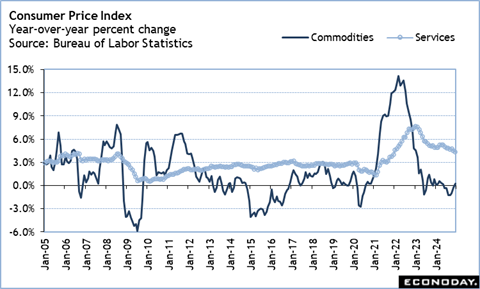

In particular, the December CPI could incline a Fed policymaker to think that while overall inflation is a little worse, core inflation is a little better. Parsing out the nuances of the softening – but still elevated – upward price pressures for services versus the flattening out in disinflation in commodities is tricky. This may be especially so with every indication that consumers are going to be hit with higher prices for foods and energy, and big ticket items likes motor vehicles and appliances. Shelter costs may be edging down overall, but events like the widespread destruction of housing in California could mean a big impact on regional rental costs that spills into the national numbers. Bitter cold and series of disruptive storms in January will probably use up inventories of seasonal merchandise which retailers will have less reason to discount. Supply chains are having trouble moving goods, which in turn could mean shortages and higher costs for other items.

Prospects for further progress on inflation seem blunted in the near term. This is reflected in some measures of inflation expectations. While overall expectations remain in line with the last year or so, these are less favorable and will speak to the FOMC about a need to ensure that there is no let up in fighting inflation. Communications from policymakers will reiterate their commitment to bringing inflation down to a sustainable level and using all their tools – basically interest rate policy and forward guidance – to do so.

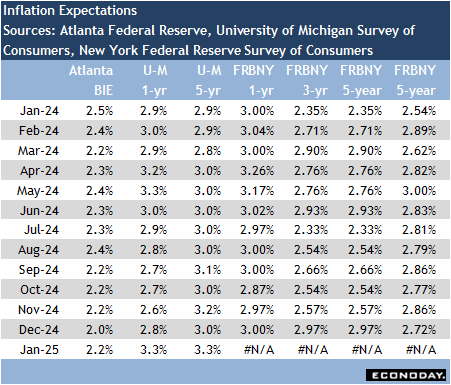

Note that in January, the Atlanta Fed year-ahead business inflation expectations report had a two-tenths increase to 2.2 percent, rising from 2.0 percent in December which was the lowest since 1.9 percent in December 2020. The implication is that businesses do expect the Fed to bring inflation down, but maybe not as quickly as previously expected. The University of Michigan 1-year inflation expectations measure is up five-tenths to 3.3 percent in January and is its highest since 33 percent in May 2024. Much of that is probably due to sticker shock on prices for eggs and poultry related to the outbreak of avian flu. Cut it does indicate that consumers see significant erosion of improvements in inflation.

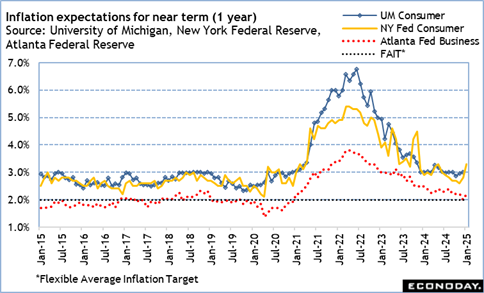

Short-term inflation expectations tend to be more volatile and particularly react to fluctuations in food and energy costs. Policymakers pay more attention to those in the medium-term which could be interpreted as a roughly 5-year timeframe.

The University of Michigan 5-year inflation expectations measure is up three-tenths to 3.3 percent in January from December, and has broken out of the range of 2.9-3.2 percent that has dominated since October 2022. This is above the 3.2 percent in November 2023 and November 2024. In fact, this is the highest in the current inflationary episode and will put the FOMC on alert regarding its credibility as an inflation fighter.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings.

Econoday’s Global Economics articles detail the results of each week’s key economic events and offer consensus forecasts for what’s ahead in the coming week. Global Economics is sent via email on Friday Evenings. The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day.

The Daily Global Economic Review is a daily snapshot of economic events and analysis designed to keep you informed with timely and relevant information. Delivered directly to your inbox at 5:30pm ET each market day. Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.

Stay ahead in 2025 with the Econoday Economic Journal! Packed with a comprehensive calendar of key economic events, expert insights, and daily planning tools, it’s the perfect resource for investors, students, and decision-makers.